What would happen ‘if’ a cabal of central bankers secretly agreed at G20 / Shanghai, to debase both currencies and keep rates low, so as to lift (or sustain) financial assets near or at high levels? That’s a concern the

March 21, 2016

GBPUSD: Having the pair weakened on Monday, further bear pressure should follow. On the downside, support lies at the 1.4300 level where a break will turn attention to the 1.4250 level. Further down, support lies at the 1.4200 level. Below

The 15th March Financial Times article that I rubbished in a blog post last week contained the comment: “the 1970s ‘Phillips Curve’ trade-off between unemployment and inflation is alive and well“. Unbeknownst to me at the time, since I never tune in

Simple Janet should have the decency to resign. The Fed’s craven decision last week to punt on interest rate normalization is not merely a reminder that she is clueless and gutless; we already knew that much. Given the overwhelming facts on the ground—4.9% unemployment, 2.3% core

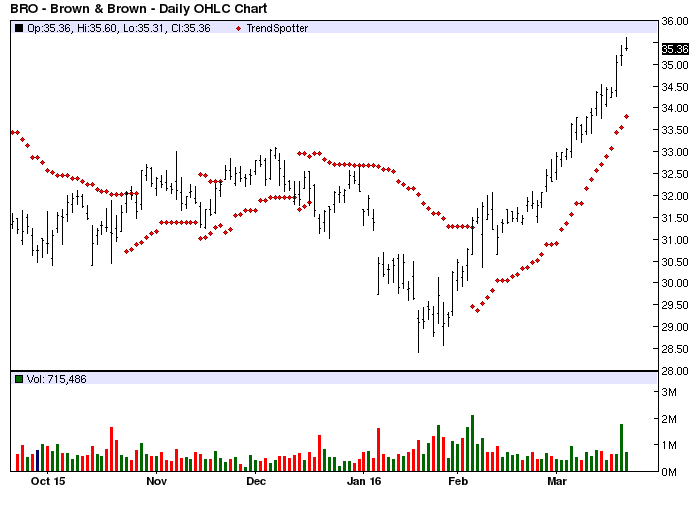

The Chart of the Day belongs to Brown & Brown (NYSE: BRO). I found the insurance brokerage by using Barchart to sort today’s All Time High list first for the highest number of new highs in the last month, then again for technical buy signals of 80%

Convertible securities have not been immune from the volatility that has roiled risk assets in 2016. However, we believe the volatile start to the year has set the stage for longer-term opportunities. A convertible bond can be thought of as

Tuesday will be a handful of announcements coming out of the European Union, and that of course can have an effect on both the Euro and the European indices. At this point, we believe that most traders will be of

Oil prices remain ebullient, relatively, compared to the dismal start to the year. Everything else, it seems, is driven by that background which means “dollar.” In that respect, we look to China or at least the Asian version of the

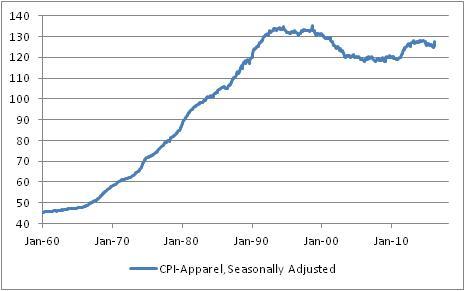

Last week, one of the curious parts of the CPI report was the large jump (1.6% month/month, or nearly 20% annualized) in Apparel. At the time, I dismissed this rise with a hand-wave, pointing out that it Apparel is only

With Japan on national holidays it was left to Shanghai and Hang Seng to show the rest of the world the way forward. With the help of the PBOC, adding ample liquidity and fixing the Yuan rate at 6.4824 (compared to