Down, down, and then down some more. As for the equities – – let’s strap ourselves in! I am (for me) in RISK OFF position, with 135% committed (when I’m super aggressive, it’s over 300%). It’s going to be quite an evening, everyone.

November 6, 2018

How about six pictures? Here are the weekly charts of the Modern Family. From top left-The Russell 2000 IWM, Transportation IYT, Retail XRT. From bottom left-Biotechnology IBB, Regional Banks KRE, Semiconductors SMH. Putting aside the midterm election, Fed minutes out

Reports Q3 revenue $364.007M, consensus $393.68M. Steve Ritchie, President and CEO of Papa John’s said, “During the quarter, we took important actions resulting in improved consumer sentiment and North America comp sales that were slightly ahead of expectations. While the

Today is the midterm election day in the US. Thanks be to God, that this is almost over, and the calls and visits and smarmy TV ads will stop, at least for a little while. The market seems to be

WTI plunged to a $61 handle, and 7-month lows, ahead of tonight’s API inventory data as trade war anxiety raised global demand fears and Iran sanctions exemptions lifted supply concerns. “Oil prices don’t have any real reason to rally significantly,” said Phil

Asia closed mixed but did see some corrections from Monday’s almost extreme moves. In Japan, the Nikkei opened around 1% better and gradually managed to build upon those gains. Although closing up 1.15% led by pharmaceuticals, industrials and commodity companies

(Audio length 00:11:10) David Erfle, The Junior Miner Junky joins me to outline the near term catalysts for the gold market. Unfortunately, most of these catalysts he sees are negative for the sector but if you employ the right strategy

A Very Defensive Bank of Canada Governor Takes Issue with His Critics Several critics, including this author[1], have taken issue with the Bank of Canada signaling that the bank rate should continue to rise to 3 percent from its current

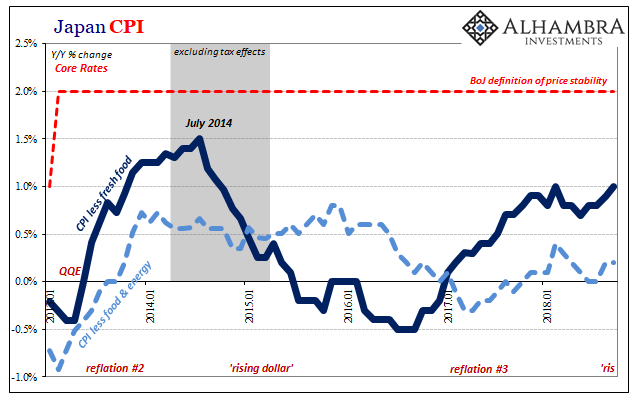

The 21st-century central banker is a unicorn chaser. This has happened by default, a product of too little success despite ever-increasing interventions. In fact, the bigger these policy intrusions become the more likely it is the central bankers will attempt

Let’s have a look at a long-term perspective on Treasury yields as of the October 26 close. The chart below shows the 10-Year Constant Maturity yield since 1962 along with the Federal Funds Rate (FFR) and inflation. The range has