A little over a week ago, I explained why I put the Mexican peso and the Canadian dollar (FXC) on shorter leashes. Canada’s extremely strong second quarter GDP report at the end of August just loosened that leash a little.

Statistics Canada reported 2Q real GDP growth of 1.1%. The annualized growth rate of 4.5% was a blistering pace that hurtled the real GDP 2Q growth in the U.S. of 3.0%. Combined with the strong growth in the first quarter, Canada experienced its strongest first half of a year since 2002. Given this growth occurred during a period of generally declining oil prices, it seems the Bank of Canada succeeded with its strategy of cutting rates earlier. It also seems that the Bank may need to soon talk of “normalizing” monetary policy although I doubt it will rush to hike rates in its next decision on monetary policy this Wednesday, September 6th.

Economic growth in Canada has soared off the period where recession seemed around the corner and the Bank of Canada was cutting rates toward zero.

Source: Statistics Canada

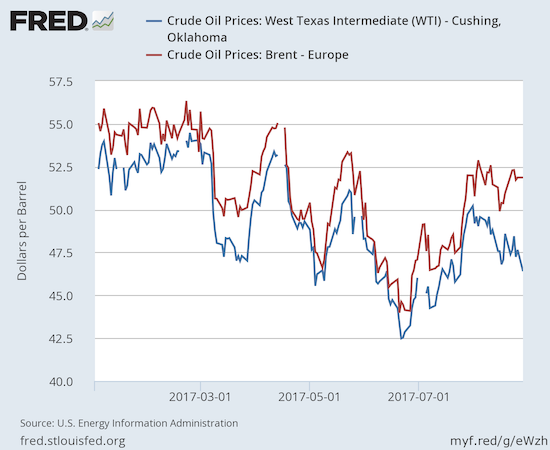

Oil prices are down year-to-date, especially for West Texas Intermediate (WTI).

Source: U.S. Energy Information Administration, Crude Oil Prices: West Texas Intermediate (WTI) – Cushing, Oklahoma [DCOILWTICO], Crude Oil Prices: Brent – Europe [DCOILBRENTEU], retrieved from FRED, Federal Reserve Bank of St. Louis, September 3, 2017.

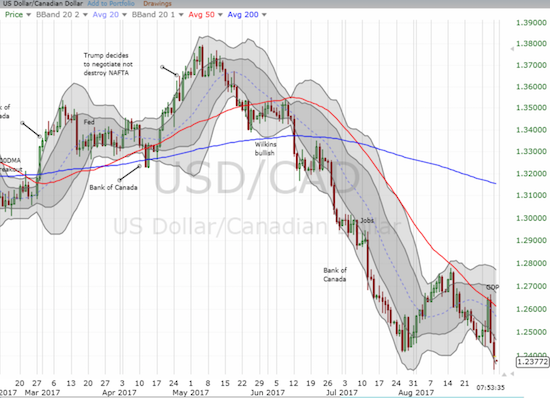

The currency market responded decisively to the strong GDP report. USD/CAD is now trading at a 2-year low.

The afterglow of the 2Q GDP report helped push USD/CAD to a 2-year low.

Source: FreeStockCharts.com

Since quickly ramping back to a net bullish position on the Canadian dollar in July, speculators have held net long contracts steady. Current levels were last seen in early 2013 but are still nowhere near the “maximum bullish” levels of 2012. Speculators have plenty of runway to get more bullish.

Speculators are holding net long contracts on the Canadian dollar at a 4 1/2 year high.

Source: Oanda

Leave A Comment