Back at the top of the year, we wrote ETF prescriptions for the higher interest rate and inflation environment likely to emerge under the new administration (see “ETFs For High Rates And Inflation,”). Of the 11 ETFs we highlighted, none were gold portfolios.

Why, several people asked me, did we forget bullion? Isn’t gold an inflation hedge? After all, they tell me, an ounce of the stuff buys a man’s suit today, just as it would have back in the time of the Caesars.

That’s another way of saying that gold’s price is highly correlated with inflation. Perhaps in the long run, but whose investment horizon stretches out two millennia? If I look at contemporary data, I see a tighter correlation to real yields.

Real yields?

Interest rates become “real” when they’re compared to the breakeven inflation rate. What do we mean by “breakeven inflation”? It’s the inflation rate implied by comparing the yields of conventional Treasury securities and Treasury Inflation-Protected Securities (“TIPS”) of similar maturity. So, yes, inflation figures into the relative value of gold, but only indirectly.

When appreciation in the Consumer Price Index (“CPI”) rises above the breakeven inflation (“BEI”) rate, you’re better off buying TIPS than conventional Treasurys.

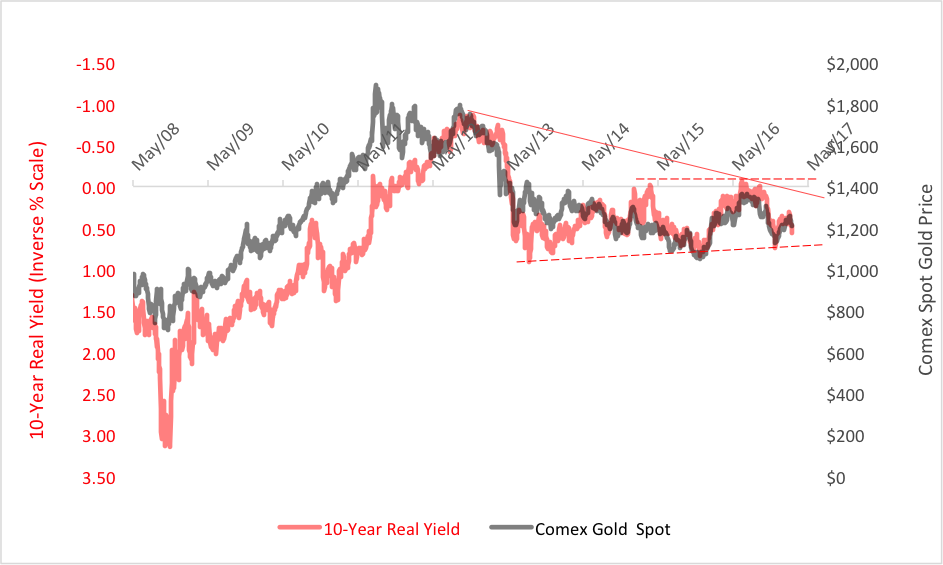

If nominal Treasury yields rise faster than the inflationary expectations reflected in the BEI, real yields rise. Historically, that’s been bearish for gold. When, on the other hand, T-note rates lag the BEI, real yield fall and gold rises. You can see this trend play out in the chart below which puts the price of gold up against the inverse of the 10-year real Treasury yield.

Notice the coincidence? When real rates decline, as they did through September 2012, gold was propelled higher. A precipitous hike in real yields that followed through June 2013 was accompanied by a $600 drop in gold’s price.

Leave A Comment