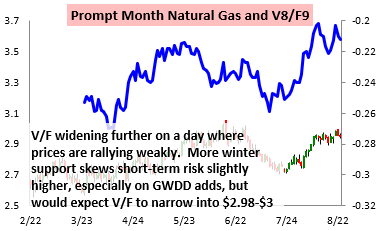

September natural gas prices were falling on weak cash prices ahead of this morning’s EIA print, but a reported injection that was just a touch below expectations helped prices find support and settle slightly higher on the day.

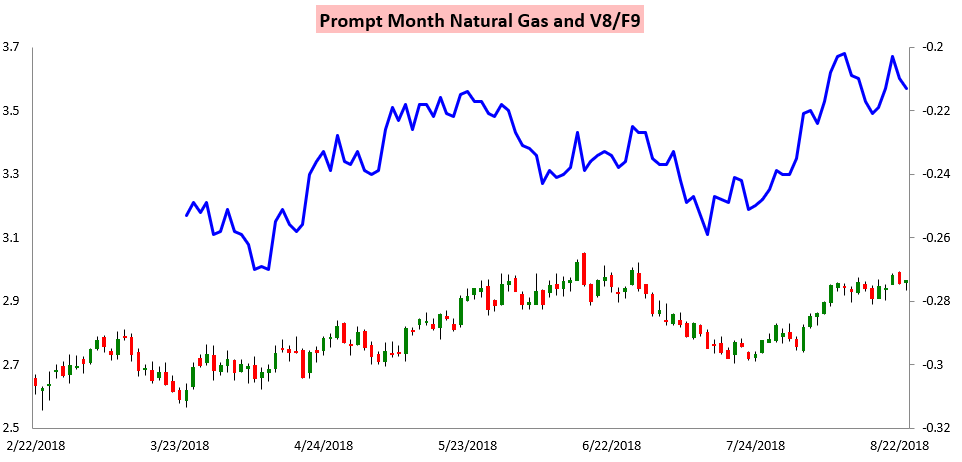

The role of the print was seen in a stronger winter strip relative to the fall or spring strip as concerns about low storage levels for the upcoming winter remained.

The result was a tick wider in the V/F October/January contract spread.

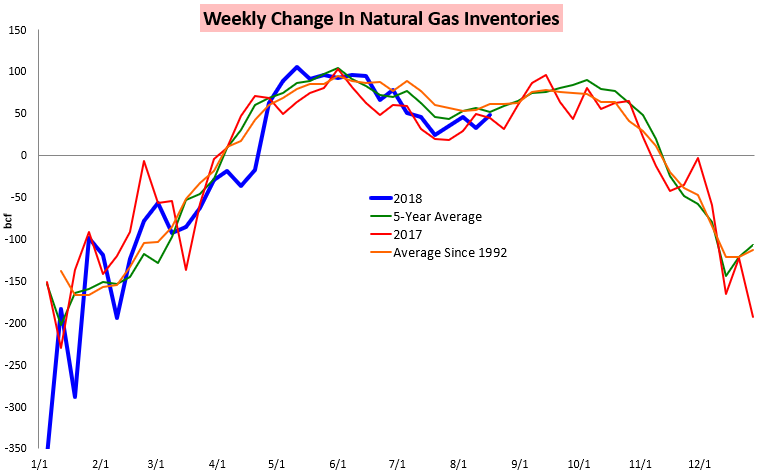

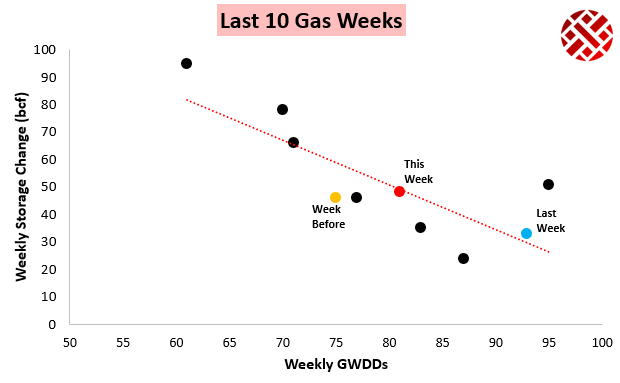

The EIA reported a build of 48 bcf last week, which was 4 bcf below both our estimate and the 5-year average of 52 bcf.

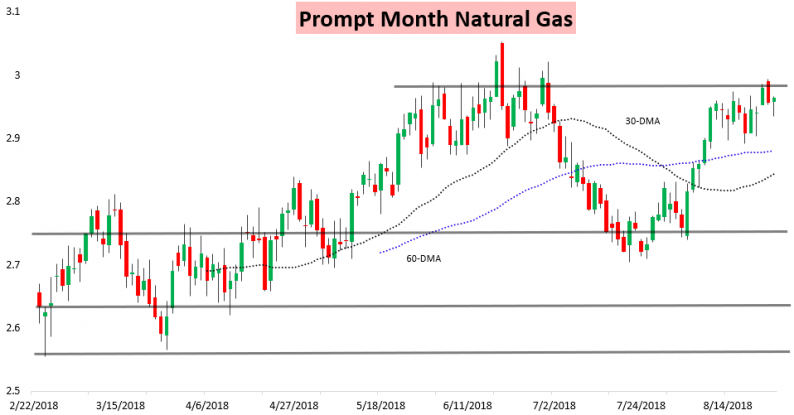

After the print in our Note of the Day we saw a more supportive natural gas strip that had us seeing our resistance level around $2.98 in play, though we highlighted that a narrowing V/F into it would likely keep it firm.

Immediately after the EIA print we released our EIA Rapid Release, where we updated our EOS forecast and models, calculated the weather-adjusted supply/demand balance of the last week, and indicated how the print fits into historical context in Gas Week 33. We saw that the print was clearly tighter than two weeks but not quite as loose as last week.

Leave A Comment