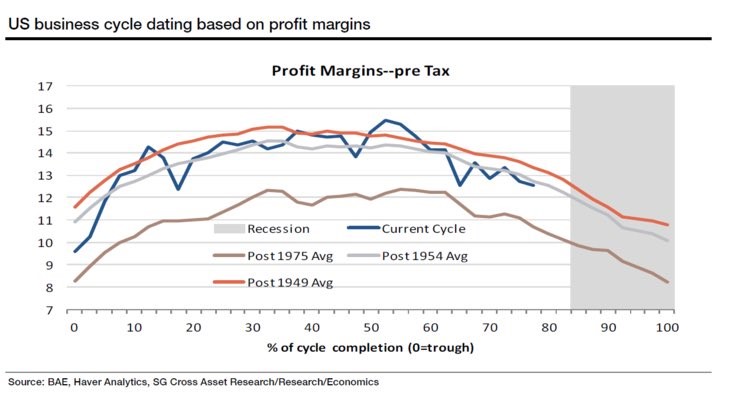

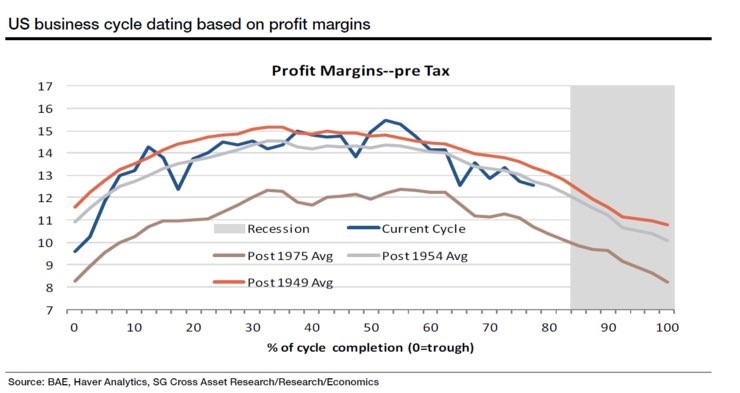

The chart below is interesting because it appears that profit margins are near their current peak. I expect Q3 margins to be down, but that’s only because of hurricane related weakness. My inkling is that the numbers here might be different because they are pre-tax margins. The stats I look at are all after taxes. On the one hand, tax shenanigans shouldn’t misdirect analysis of corporate profits. On the other hand, if taxes are cut in the next few months, profits will benefit making this chart null and void. Assuming taxes aren’t cut, this chart puts the economy close to a recession. If you assume we’re at peak margins, that puts off a recession for a year or two.

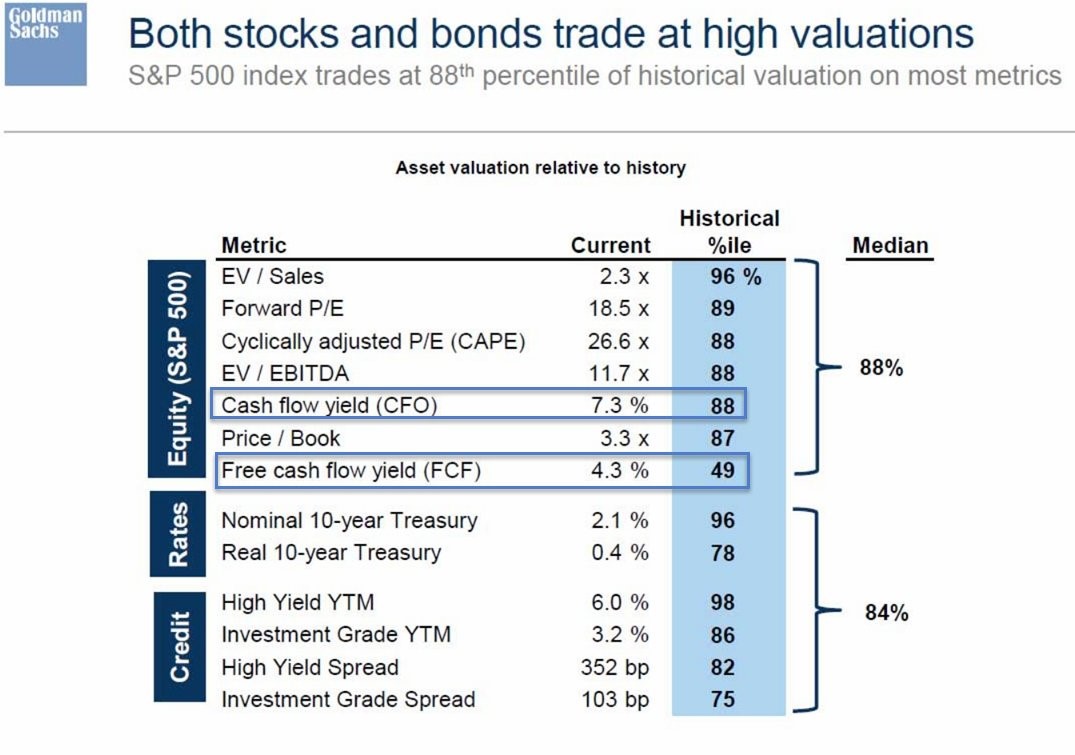

In a previous article we discussed how many asset classes such as bonds, stocks, and currencies have had very low volatility. The table below looks at different asset classes’ valuations. As you can see, when you combine a few metrics, stocks are in the 88th percentile in terms of valuation. The real treasury yield is closer to its average price than the nominal treasury yield because inflation is so low. Both high yield debt and investment grade debt are more expensive than average. High yield debt is extremely overbought because investors are looking for an alternative to stocks. Anything with high risk is on fire even if it doesn’t offer much return. Stocks which have high multiples appear like they’re fully priced, but they continue to move higher, so maybe our perception of what is fully valued is wrong. The other possibility is speculation has gotten excessive.

The chart below breaks down the credit spreads by rating. To be clear, triple B is the best on this list and triple C is junk. It’s also worth noting that the percentiles are the opposite as the table below. The lower the percentile, the more expensive the asset is. The reason for that is lower spreads mean yield differences are lower. This means investors don’t generate much more return for the extra default risk they are taking by buying low rated debt. Surprisingly, double B is the most expensive while triple C is the least expensive. I say it’s surprising because in this risk on environment, you’d expect the worst rated bonds to do the best. Junk bonds are performing well, but on a historical scale they’re only in the high 30s percentile.

Leave A Comment