Earlier this week, we updated our commentary on household income distribution to include the Census Bureau’s release of the 2017 annual data. Our focus was on arithmetic mean (average) household incomes by quintile (and the top 5%) over the 50+ year history of this data series. The analysis offered some fascinating insights into U.S. household incomes.

But the classification misses the implications of age for income. Households are by no means locked into the same quintile over time. Young educated households with professional skills and aspirations will typically move into the higher earning brackets during their financial life cycles. Households dependent on income from unskilled labor and non-professional service employment will not see the same financial progress over the years.

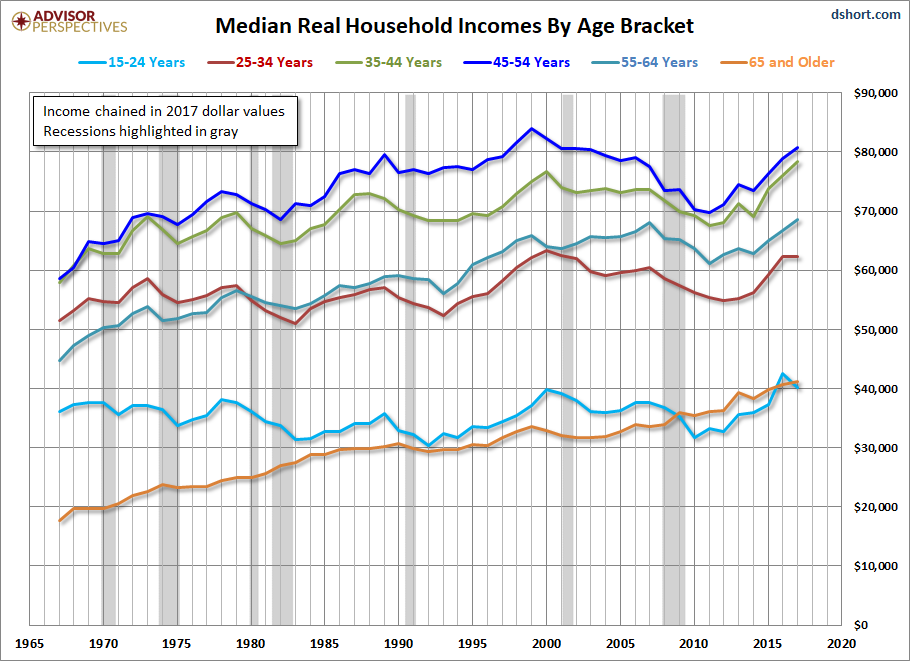

So let’s review the household income data another way, this time focusing on the incomes by the age bracket. The data we’re analyzing is the median (middle) household income the age brackets for the heads of household (see Table H.10 for all races).

Because this is a longitudinal analysis across nearly five decades, including the stagflation of the 1970s, we’ve used the Census Bureau’s real (inflation-adjusted) series chained in 2017 dollars based on a research variant of the Consumer Price Index, the CPI-U-RS. In other words, the incomes in earlier years have been adjusted upward to the purchasing power of the most recent year in the series.

The first chart shows real household incomes of the six age brackets.

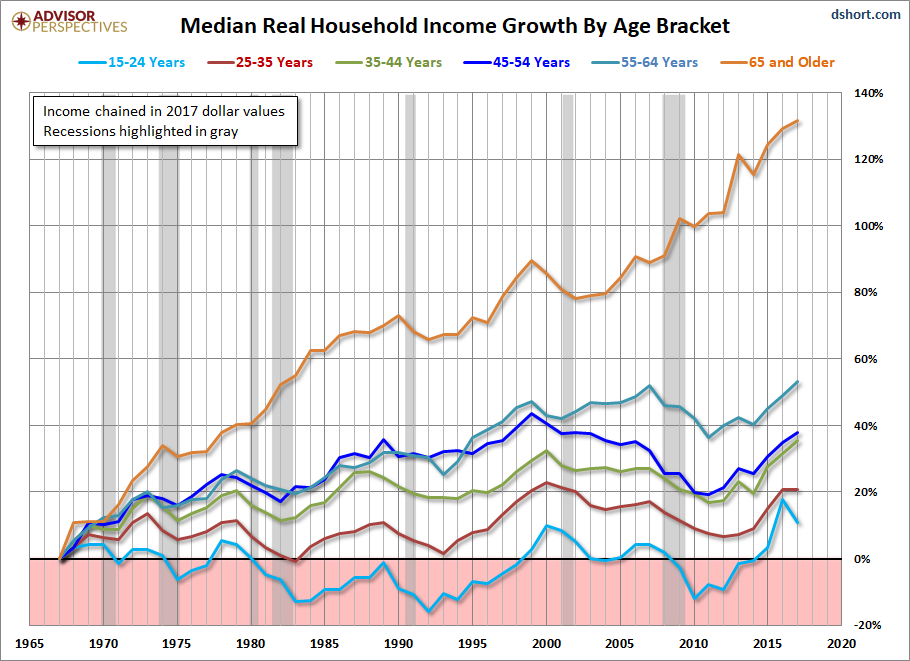

But more revealing is a comparison of the cumulative real growth of median incomes for the six age brackets.

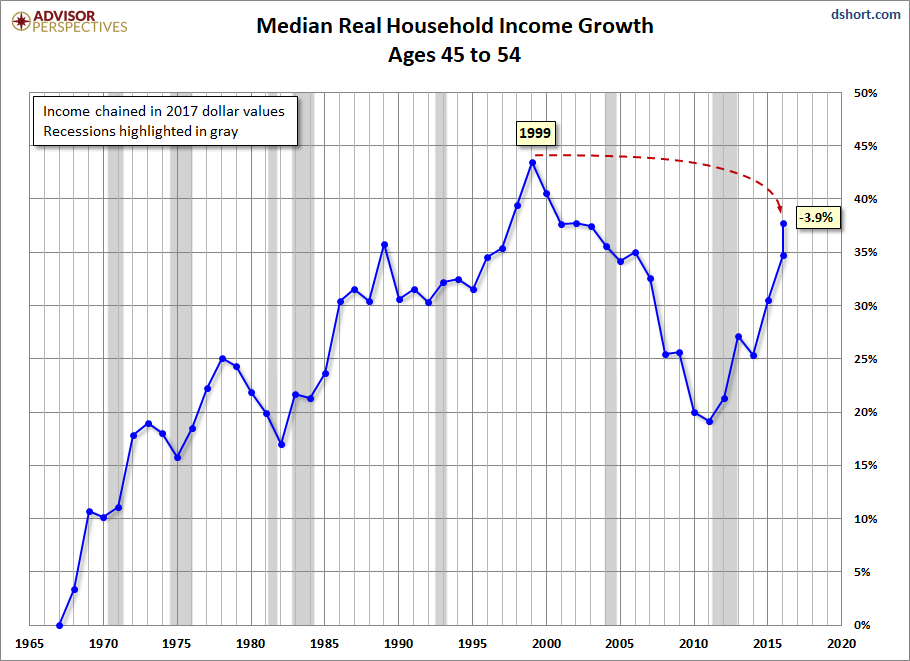

Let’s focus on the plight of the peak earning age bracket, ages 45-54.

There are some immediate observations we can make about these charts:

Leave A Comment