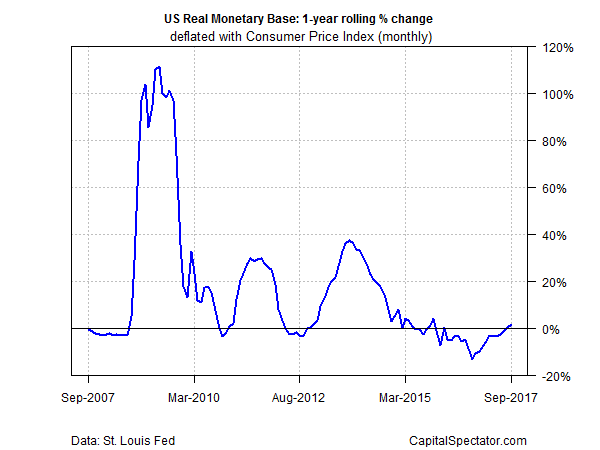

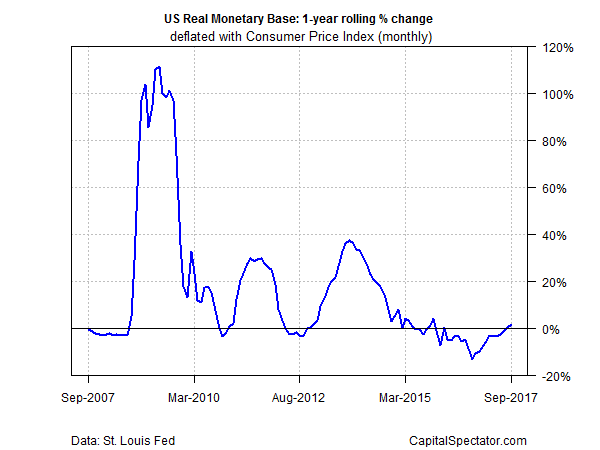

Federal Reserve officials have been talking up the odds of another hike in interest rates and the Fed funds futures market is pricing in a near certainty of no less for the December monetary policy meeting. But the case for tighter policy may not be as strong as it appears, based on the latest data for M0’s real (inflation-adjusted) year-over-year change.

The Fed’s narrowest gauge of money supply – aka M0, the monetary base, or “high-powered” money – continued to rise in September vs. the year-earlier level in real terms. The 1.4% advance follows August’s 0.3% rise — the first run of back-to-back increases in nearly two years. The implication: the central bank’s actions don’t yet match its hawkish comments of late.

Note that the contraction in M0 reached a trough a year ago, in October 2016, when the decline rate reached -13.4%. Since then, the negative year-over-year trend has been fading, moving into positive terrain in August and September. This history alone doesn’t discount another rate hike, but it’s a trend that bears monitoring as new data is published ahead of the Fed’s Dec. 12-13 FOMC meeting.

History tells us that M0’s inflation-adjusted annual trend offers a rough proxy for measuring the Fed’s monetary policy in real time. For example, the real M0 annual trend offered a clue in early 2015 that the Fed was close to tightening policy for the first time in nearly a decade. Later that year, in December 2015, the central bank announced that it was raising the target range for the federal funds rate. The central bank has increased rates several times since then. The question is whether the hawkish bias will roll on?

The crowd is convinced that the future is clear. Fed funds futures are currently pricing in a 97% probability that the Fed will increase rates again in December, based on CME data for this morning.

Leave A Comment