With the market now stuck in the “Icarus Rally” melt-up predicted earlier in the year by BofA Michael Hartnett, in which EFTs, algos and desperate carbon-based hedge fund managers are all chasing performance, i.e. beta, in the last weeks of the year, at least until the inevitable “Humpty Dumpty great fall“, some have been naive enough to ask just how overvalued are stocks as of this moment.

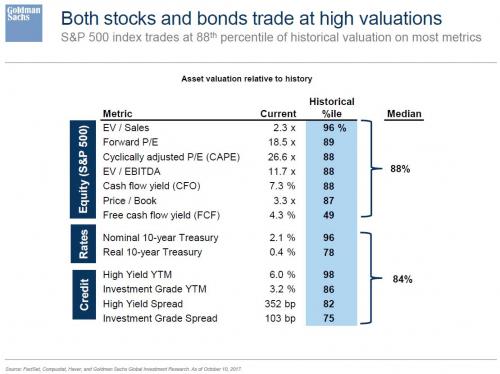

Yesterday we showed one answer, when according to Goldman Sachs, the average stock is in the 88th percentile of all historical valuations and 98% from if one uses median stocks to eliminate huge outliers such as Apple; the number would be even higher if one excluded cash flow-based valuation metrics, which are artificially boosted due to the collapse in capex and investment spending.

In any event, it is safe to say that stocks have never been more expensive.

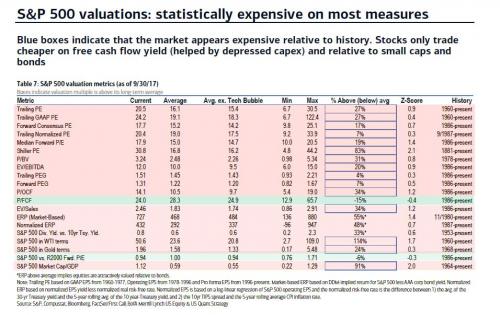

Today, we present a different response, this time from Bank of America, which has just completed the periodic update of its valuation matrix based on the 20 most widely used valuation metrics, and which finds that as of today, the S&P is substantially overvalued on 18 of 20 valuation metrics, with the only exceptions being free cash flow (helped again by depressed capex), and relative to small caps/bonds – the Fed’s favorite indicator -where yields remain depressed thanks to the Fed’s failure to stimulate wage inflation for nearly 9 years.

Some brief observations from BofA: the S&P 500 forward P/expanded to 17.7x in October – its highest level in 13½ years — as the market rallied more than estimates climbed. The valuation backdrop for the S&P 500 remains the same: US stocks trade above historical average levels across nearly all metrics, but equities continue to look attractive relative to bonds, where the equity risk premium (ERP) is more than 50% above its long-term average. Multiples expanded across most sectors last month: the energy sector continues to trade at a record discount to history on relative Price/Book, but grew increasingly expensive on relative forward P/E as analysts revised down EPS estimates amid the continued weakness in oil prices.

Leave A Comment