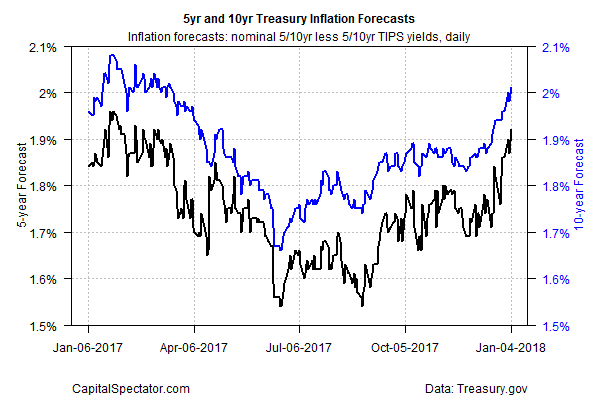

The Treasury market’s 10-year estimate of future inflation rose above the Federal Reserve’s 2% target this week – the first time that level has been breached for this maturity since last March, based on daily yield-spread data via Treasury.gov. Official inflation numbers, which are published with a lag, continue to reflect pricing pressure that’s modestly below the Fed’s target. The Treasury market, however, is betting that inflation will accelerate this year.

The implied inflation forecast based on the yield spread for the nominal 10-year Treasury less its inflation-indexed counterpart ticked up to 2.01% on Thursday (Jan. 4), the highest level in ten months. The current 5-year Treasury inflation forecast is slightly lower at 1.92%, although that’s a 10-month high too.

Firmer inflation estimates in Treasuries align with comments in the Fed minutes for Dec. 12-13 FOMC meeting, when the central bank lifted interest rates for the fifth time since the recession ended in 2009. The latest minutes, published earlier this week, advise:

Many [Fed participants] indicated that they expected cyclical pressures associated with a tightening labor market to show through to higher inflation over the medium term. These participants generally judged that much of the softness in core inflation this year reflected transitory factors and that inflation would begin to rise as the influence of these factors wane

The Treasury market agrees. Indeed, the policy sensitive 2-year yield has been climbing sharply in recent months, rising to 1.96% yesterday – the highest since 2008. That’s a sign that the bond market is convinced that more rate hikes are coming in the months ahead.

Trend analysis of the 2- and 10-year yields implies that rates will continue to increase in the near term. For example, three exponential moving averages (EMA) for the 2-year rate reflect a strong upside bias, based on the 50-day EMA that’s well above the 100-day EMA, which is above the 200-day EMA.

Leave A Comment