As I noted in yesterday’s missive, Yellen’s recent testimony on Capitol Hill sent robots frantically chasing asset prices on Thursday even before testimony began. The catalyst was the release of prepared testimony which included this one single sentence:

“Because the neutral rate is currently quite low by historical standards, the federal funds rate would not have to rise all that much further to get to a neutral policy stance.”

And on that statement, doves flew and algorithms kicked into to add risk exposure to portfolios. Why? Because she just said that rates will remain low forever. As my partner, Michael Lebowitz, noted yesterday:

“Per Janet Yellen’s comment, the ‘neutral policy stance’ is another way of saying that the Fed funds rate is appropriate or near appropriate given current and expected future economic conditions. Said differently, Janet Yellen is admitting what we’ve been saying for years – the economy has been stagnant, is stagnating and will continue to stagnate.

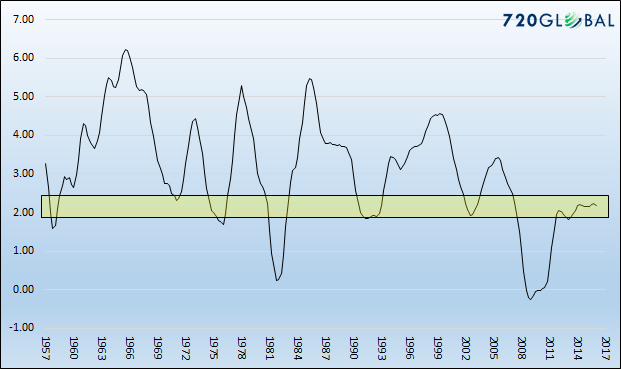

If we assume that Yellen is referring to a range of 1.25-1.75% as an appropriate Fed Funds rate, based on statistical analysis of data since 1955, we forecast that real GDP growth rate is likely to average somewhere between 2.00-2.50% for the foreseeable future. For perspective, the graph below plots the range of expected GDP growth vs historical secular (3-year average) GDP growth. In years past, such a slow rate of growth (highlighted in yellow) was considered nearly recessionary.”

The problem, of course, is that a 2% economic growth rate is not conducive to a strongly expanding economic environment and does not support current market valuations. The first chart below compares the cumulative growth rate of the real S&P 500 as compared to GDP. The great “bull markets of the 50’s and 60’s, the 80’s, and now the 10’s have all previously ended when the growth of the S&P 500 exceeded the growth of the economy.

Leave A Comment