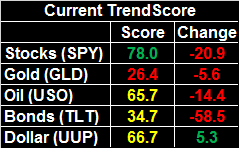

Yikes. Last week’s setback was the worst weekly loss for the market since March… a factoid made even more alarming by the fact that we only saw four trading days last week. One more day could have upped the ante on the “worst since” accolade.

And yet, it can’t be ignored that last week’s lull also followed an oddly strong finish to August; there was lots of profit-taking potential on the table. In fact, there was so much froth, even with the 1.0% tumble the S&P 500 took last week, it’s still not worked its way into real technical trouble… not that September is the month in which the bulls want stave off a selloff.

We’ll look at what the market did right and wrong last week below, as always. First, however, let’s run down last week’s and preview this week’s economic announcements. With no major earnings announcements in store, investors will be grasping onto other data nuggets.

Economic Data

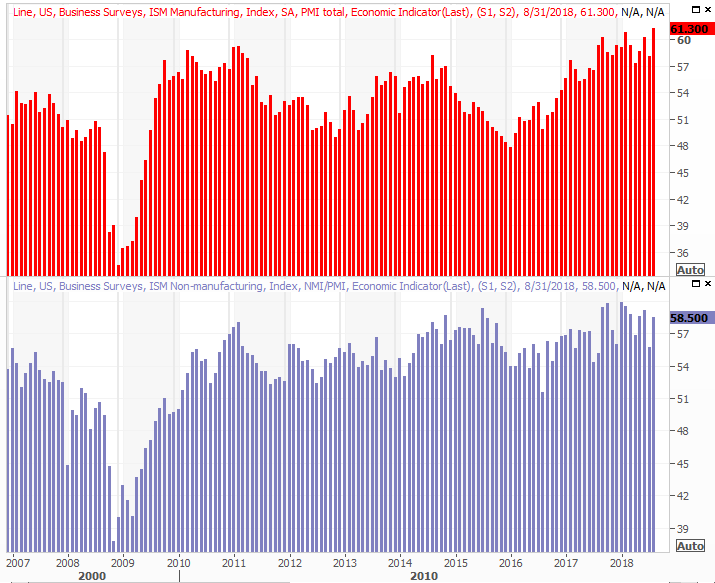

Last week was chock full of economic reports, with the biggest of them being the grand finale… Friday’s jobs report for the month of August. There was plenty of other information worthy of recapping though, beginning the ISM data. Tuesday’s ISM Manufacturing Index rolled in at 61.3, well above expectations and up to a multi-year record. Thursday’s ISM Services Index report wasn’t quite as impressive, though the print of 58.5 was still up, and better than forecast.

ISM Index Charts

Source: Thomson Reuters

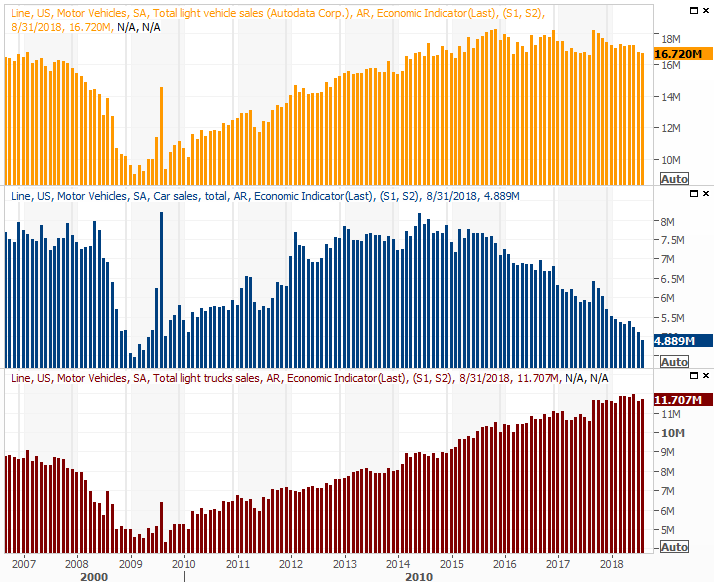

Also on Tuesday we heard about August’s automobile sales… a mixed bag. Passenger vehicle sales fell (again), though truck sales grew. In total though, the annualized pace fell again, to 16.72 million. That’s the second-lowest reading in a couple of years, and the broad downtrend is still in place. It’s also not as if truck sales are blistering.

Automobile Sales Charts

Source: Thomson Reuters

Leave A Comment