FUNDAMENTAL FORECAST FOR GOLD: NEUTRAL

Talking Points:

Still no sign of a breakout for Gold with prices inching lower by 0.5% for the week, marking the 1st weekly decline since late March. Renewed buying for the DXY as US treasury yields pick and easing geopolitical tensions see the precious metal failing to hold above $1350 yet again in what has been another rangebound week.

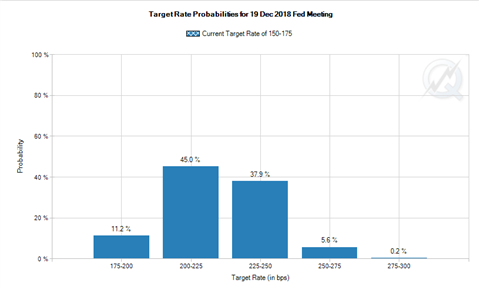

The recovery in the USD-index has begun to pick up the pace, testing the psychological 90.00 level amid the rise in US treasury yields with the 10Y hitting highs of 2.94%, subsequently denting the appeal of the non-interest yielding bullion. The continued rise in global commodity price index (led by oil and aluminum), alongside rising price pressures (Philly Fed prices paid highest since 2011) in the US economy have thus raised inflation expectations, consequently steepening the priced-in Federal Reserve rate hike view. According to the latest CME FedWatch, markets are pricing in a near 44% chance of a further 3 rate hikes by the end of the year.

Source: CME

Easing geopolitical tensions sapped demand from the safe-haven asset with newsflow regarding the latest in Syria on the quiet side, while reports that North Korea are willing to listen to calls of denuclearization on the Korean Peninsula.

NEXT WEEK’S ECONOMIC CALENDAR

Given that we enter the blackout period meaning that no Federal Reserve members will be speaking on the economy or monetary policy, alongside a light economic calendar until the end of the week, it is likely that gold prices will be trading in somewhat sideways fashion for a large part of the week.

Much of the focus for gold traders will be on the upcoming US data towards the back end of the week. On Thursday we will see the release of the politically sensitive trade balance figure, in which the trade deficit is expected to marginally rise to $75.5bln from $75.4bln. A figure that shows a considerable rise in the trade deficit and in particular with China would unlikely ease the current trade tensions between the US and China, as such an air of caution over trade spats could thus keep the precious metal elevated. At the back end of the week, eyes will be on the first reading of the US Q1 GDP report which is expected to show a sizeable moderation to 2% from 2.9%.

Leave A Comment