I recently wrote an article for Sure Dividend entitled “Consider Equity REITs for Your Next Investment“. In that article, I listed nine equity REITs for dividend investors to consider in light of the drubbing that REIT valuations have recently taken due to fear of rising interest rates and to capitalize on the pass-through provision for REIT income included in the new tax legislation. Both of these topics are covered in some detail in the previous article. This article provides a more complete investment thesis for Omega Healthcare Investors (OHI), one of the nine REITs highlighted in the previous article.

Omega Healthcare Investors

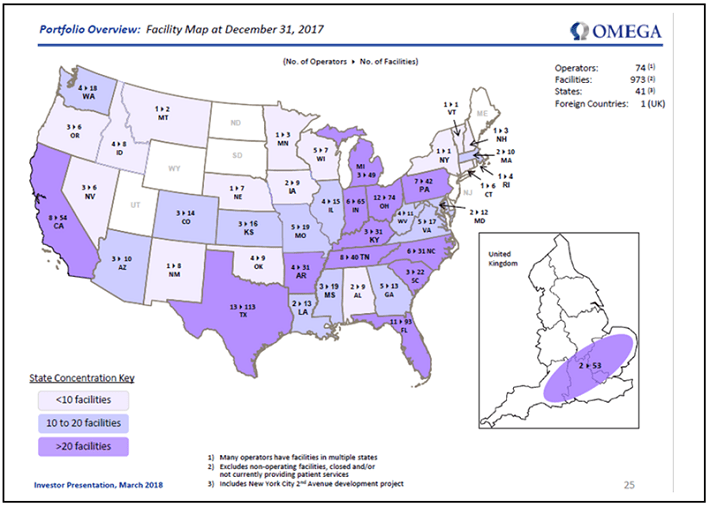

Omega invests primarily in skilled nursing facilities (SNFs) and is as close to a pure play SNF REIT as can be found in the market with 83% of revenues generated through ownership of SNF facilities and 17% generated by senior housing developments. The company’s enterprise value is $10.3B making it the largest SNF focused REIT in the market. Omega owns 973 facilities located in 41 states and the United Kingdom (UK) managed by 74 different operators.

Source: OHI Investor Website

The chart above shows OHI has reasonable geographic diversification with facilities across most of the US and a foothold in the UK. As noted above, OHI also has a diverse set of 74 operators for its facilities. The chart below provides details for the top 10 based on OHI revenue generation.

Source: OHI Investor Website

Readers will note that the top 10 operators of OHI’s facilities provide roughly 65% of OHI’s revenues.

Omega carries an investment grade credit rating of BBB- from Standard & Poor’s and Fitch. To maintain that investment grade credit, OHI carries a fairly conservative debt load with a total debt to EBITDA ratio of 5.1x and a fixed charge ratio of 4.1x ensuring that OHI generates more than sufficient earnings (EBITDA) to cover the interest on debt plus preferred dividend distributions. Omega also has sufficient liquidity with a $1.25B revolving credit facility with roughly $1B available as of February, 2018.

Omega Healthcare’s Recent Financial Performance

Omega’s past financial performance has been just short of exceptional, particularly for a stodgy conservative equity REIT. The chart below shows OHI’s investment and revenue growth from 2004 through 2017.

Source: OHI Investor Website

Both investments and revenue have grown at better than 19% annually for the last 14 years. That growth in investments and revenue has also translated into solid growth in EBITDA and Adjusted Funds From Operations (AFFO) over the same period.

Leave A Comment