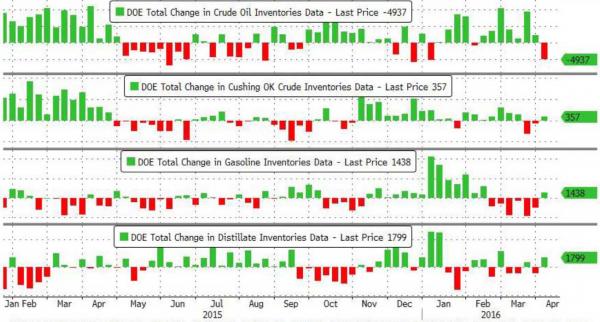

Following yesterday’s API data, which showed the biggest draw of 2016 with a 4.6 million reduction in oil inventories, everyone was keenly looking forward to today’s DOE data. Moments ago the DOE indeed confirmed the API data, reporting that in the past week oil inventories declined by 4.949MM, more than the API print, down from last week’s 2.3MM and well below the expected 2.850MM increase.

This was the largest draw since the first week of January.

However, while in the recent past the crude builds were offset be declines in gasoline and distillate reductions, this time it was a mirror image, as first Gasoline rose by 1.438MM, above the -1.1MM draw, while Distillate increased by 1.799MM, above the -850K draw expected.

This happened even as Refinery utilization rose 1.0% W/W, above the 0.35% expected, operating at a 91.4% of capacity in the past week.

As a result Cushing holdings rose by 0.3MM, rising to 66.3MM barrels and once again approaching its operational capacity.

Some more headlines from the report:

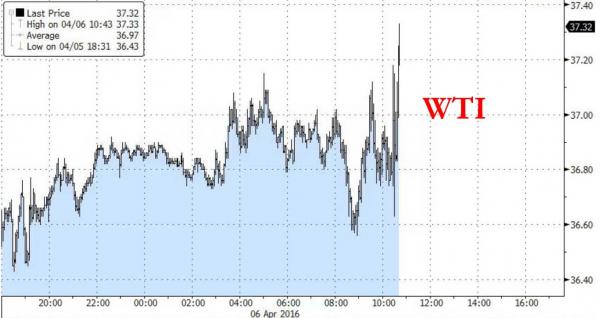

On the news, oil initially spiked on the draw headline, then erased all gains focusing on gasoline and distillate build, and then soared for the second time rising as high as $37.40 as algos focused on all those things they ignored in previous DOE reports.

Leave A Comment