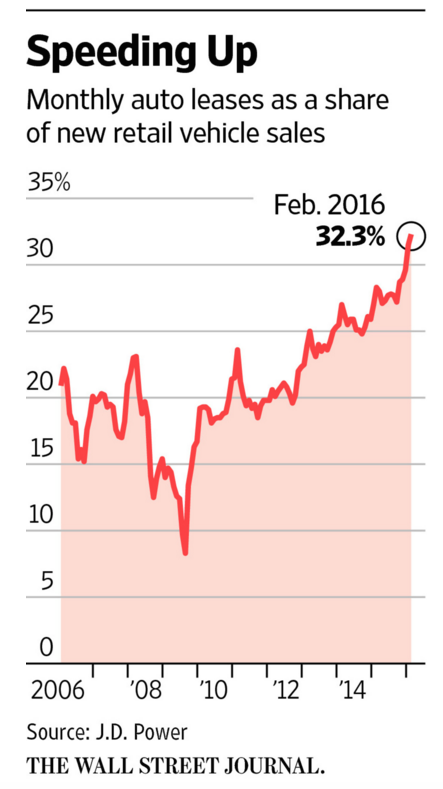

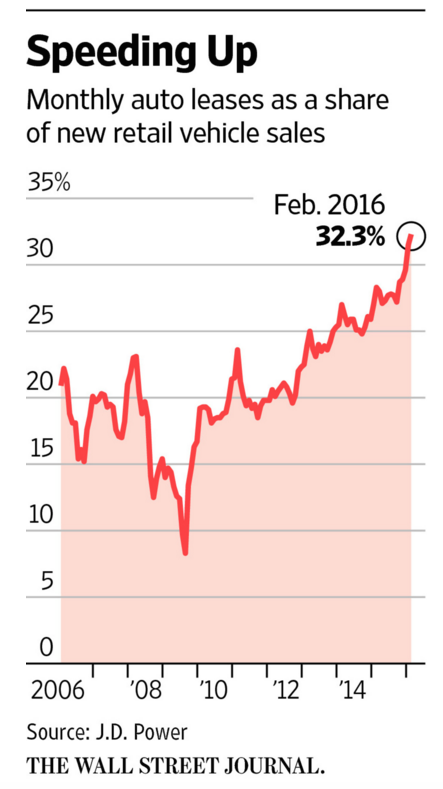

Last week, we learned that vehicle leasing as a percentage of monthly light-vehicle sales hit a record in February at 32.3%.

In other words, a third of the over 1 million cars and light trucks “sold” during the month were leases, according to J.D. Power.

This is indicative of what is now a long-term trend. Have a look at the following chart from WSJ, which shows that since 2009, the share of monthly auto leases as a percentage of vehicle sales well more than tripled:

Of course the thing about leased vehicles is that they come back, and as WSJ wrote last week, “about 3.1 million vehicles will return to dealer lots off leases this year, up 20% from 2015 [and] the number will climb to 3.6 million in 2017 and 4 million in 2018.”

So what does that mean for dealers? Deflation.

And what does that mean for the automakers? Hefty losses.

Nothing about this is hard to understand. You get a supply glut causing pricing assumptions for your existing inventory to prove wildly optimistic and you end up with giant writedowns.

This has happened before. “The auto industry expanded the use of leasing in the mid-1990s, helping to fuel retail sales of new vehicles,” WSJ recounts. “Eventually, a glut of off-lease cars sent resale values down and auto lenders who had bet residuals would remain high ended up racking up billions of dollars in losses, having to sell the cars for much less than they anticipated.”

Right. Nothing difficult to grasp about that. But the especially silly thing about the dynamic with auto leases is that it was the dealers and the automaker-affiliated financing companies that made the leases in the first place. In other words, it’s not like this was some supply shock that couldn’t have been forecast ahead of time. In fact, they knew exactly when the off-lease deluge would start, so it’s not entirely clear why they would have set optimistic residual assumptions.

Leave A Comment