In January, the ECB tapered its bond buying from €60 billion per month to €30 billion per month. Equally as important, the central bank is expected to stop its bond buying completely by September 2018. European economic growth has accelerated recently, but it’s unclear how much the economy was helped by the QE and how much it was helped by the global synchronized economic recovery. The ECB policymakers will, of course, take credit for the success. This is just like how Janet Yellen is praised for keeping the economy out of a recession as if she was the sole reason the economy stayed out of a recession rather than a piece of the puzzle.

There are some analysts and personalities who over exaggerate what the Fed and other central banks have done because drama gets people talking. The ECB’s QE certainly had an effect on the market which we’ll discuss, but it’s safe to say those predicting Armageddon when QE ends will be disappointed. Most investors already know QE will end, so if Armageddon was going to happen, it would be here already.

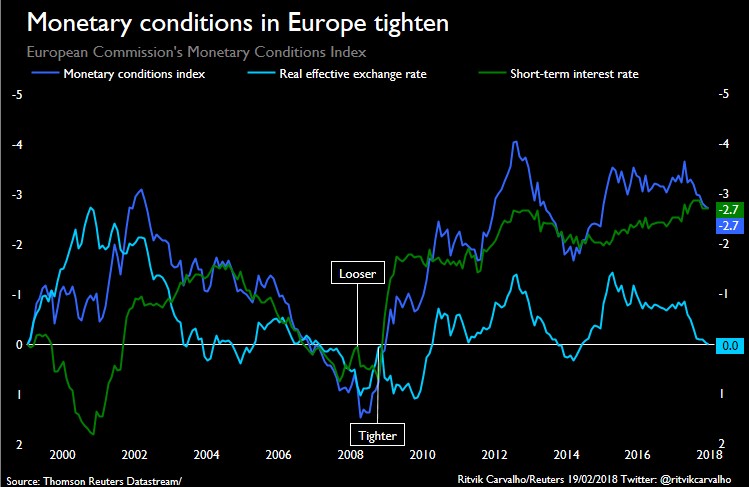

As you can see from the chart below, the monetary conditions index has tightened the most since 2014 which was right before the ECB started this round of QE.

QE Taper Causes Monetary Conditions To Tighten In Europe

As we expected, the euro strengthened versus the dollar because of this unwind. It’s larger than the Fed’s QE. The Fed is shrinking its balance sheet, while the ECB is tapering its unwind, but the rate of change is important. The Fed just went from unwinding its balance sheet from $10 billion per month to $20 billion per month. The additional $10 billion is much smaller than additional €30 billion ECB taper.

Greece Bonds Yielding Less Than U.S. Treasuries

One of the most unusual aspects related to QE is the Greek 2 year bond yield has a lower yield than the US 2 year bond. The chart below shows the historical changes.

Leave A Comment