Previous:

On Wednesday, trading on the euro/dollar pair closed up. Buyers were unfazed by positive US data and the drop on the euro/pound cross. When the euro started correcting against the British pound and US 10Y bond yields started to drop, growth on our pair gathered pace. This surge petered out at around 1.1818.

Demand for the single currency was consistent throughout the day as investors await a decision from the European regulator on tapering its asset purchasing stimulus program.

US data:

Day’s news (GMT+3):

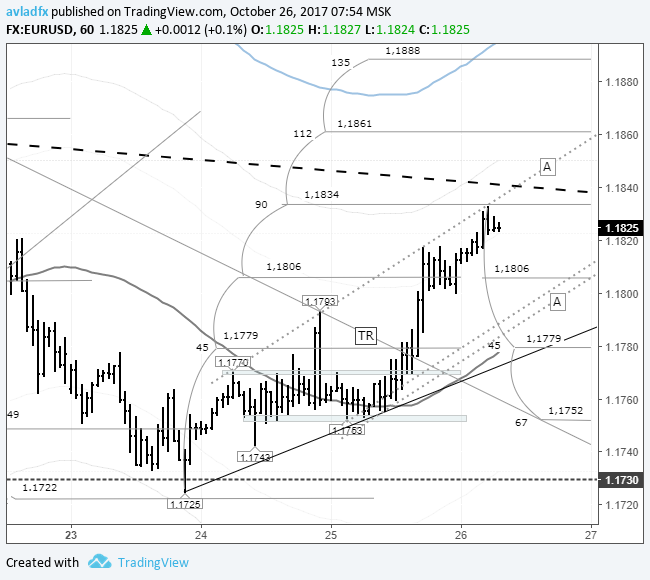

Fig 1. EURUSD rate on the hourly. Source: TradingView

My predictions for yesterday failed to manifest. Drops on the euro/pound cross, as well as on pairs involving the loonie and Aussie dollar, failed to push the euro down against the US dollar. Traders bought up euros before the ECB meeting, expecting that the QE program would be reversed. They’re expecting the regulator to announce a reduction in their asset purchasing program from 60 to 40 billion EUR a month.

In Asia, the dollar is falling across the board. The euro is moving upwards within the local A-A channel along its northern border. At the time of writing, the euro is trading at 1.1837. There’s a resistance running through 1.1840. If today’s session closes with the price above 1.1840, we can forget about a head and shoulders model forming on the daily timeframe.

Leave A Comment