What they said

“In determining whether it will be appropriate to raise the target range at its next meeting, the Committee will assess progress–both realized and expected–toward its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.”

What they did

What did the Fed do yesterday? Why, they rolled over once again and held ZIRP. They also got mighty specific with some wording that freaked out precious metals players and put in a reversal, not only in the metals, but importantly, in their ratio. See yesterday’s post on the Silver-Gold ratio’s status… What Thing Looks Like the Other. A reversal in silver vs. gold would put the sector on a correction and also issue a warning to other global markets.

So the Fed still has a few tricks up its sleeve. They are backed into a corner in which they are expected to normalize monetary policy because well, they are they Fed, they have perceived credibility (i.e. the confidence of the markets in what is largely aconfidence game) and legions of conventional investors to whom they must appear reasonably normal.

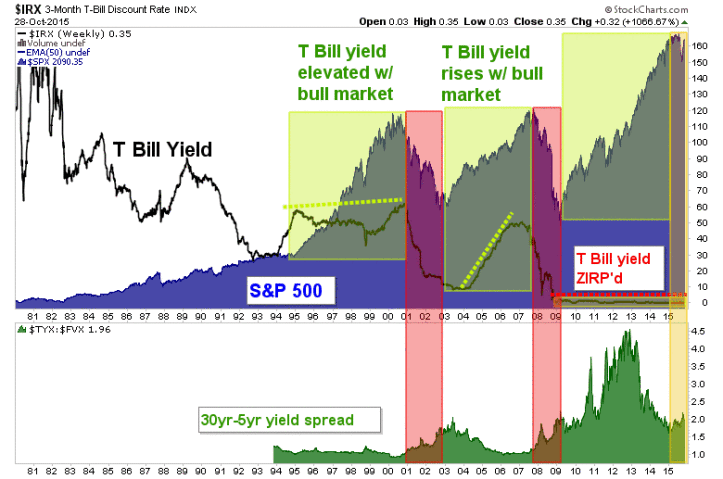

What they are facing

Here is what they actually have, an abnormal distortion of their own creation in the markets; and if you ask me, an out and out disgrace on their hands. The horizontal red dotted line is post-2008 monetary policy. This while the S&P 500 grew a third hump of epic proportions.

Looking at yields in the 30yr-5yr year range (lower panel above), we see that the Treasury bond market is trying to turn that curve up (orange shaded area). The early stages of such upturns have broken the stock market on the last two cycles (red). Is this a picture of the ‘Bond Vigilantes’ taking over the show out on the curve, far enough away from the Fed influenced short end?

Shorter-term spreads still under control

The 10yr-2yr still looks completely under control and in the grips of unbending confidence in the Federal Reserve. Here are the nominal 10’s and 2’s, showing the shorter duration popping big with the dreaded wording in the FOMC release. The Fed really really means it this time!… maybe. The alignment in bonds nearer the Fed-controlled Funds Rate continues to show that all is well, normal, in control and by the way, antagonistic to gold, which most definitely does not want to see short rates rising vs. long rates.

Leave A Comment