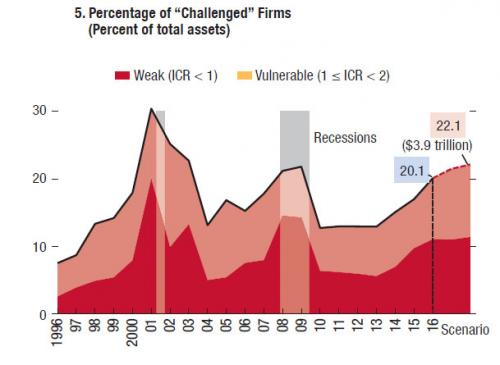

Exactly one year ago, in its Global Financial Stability report, the IMF issued a stark warning when looking at the soaring level of private sector debt: it found that more than 20% of US corporations are at risk of defaults once interest rates rise, and calculated that the combined assets of firms threatened by default – those who earnings do not cover their interest expense – could reach almost $4 trillion.

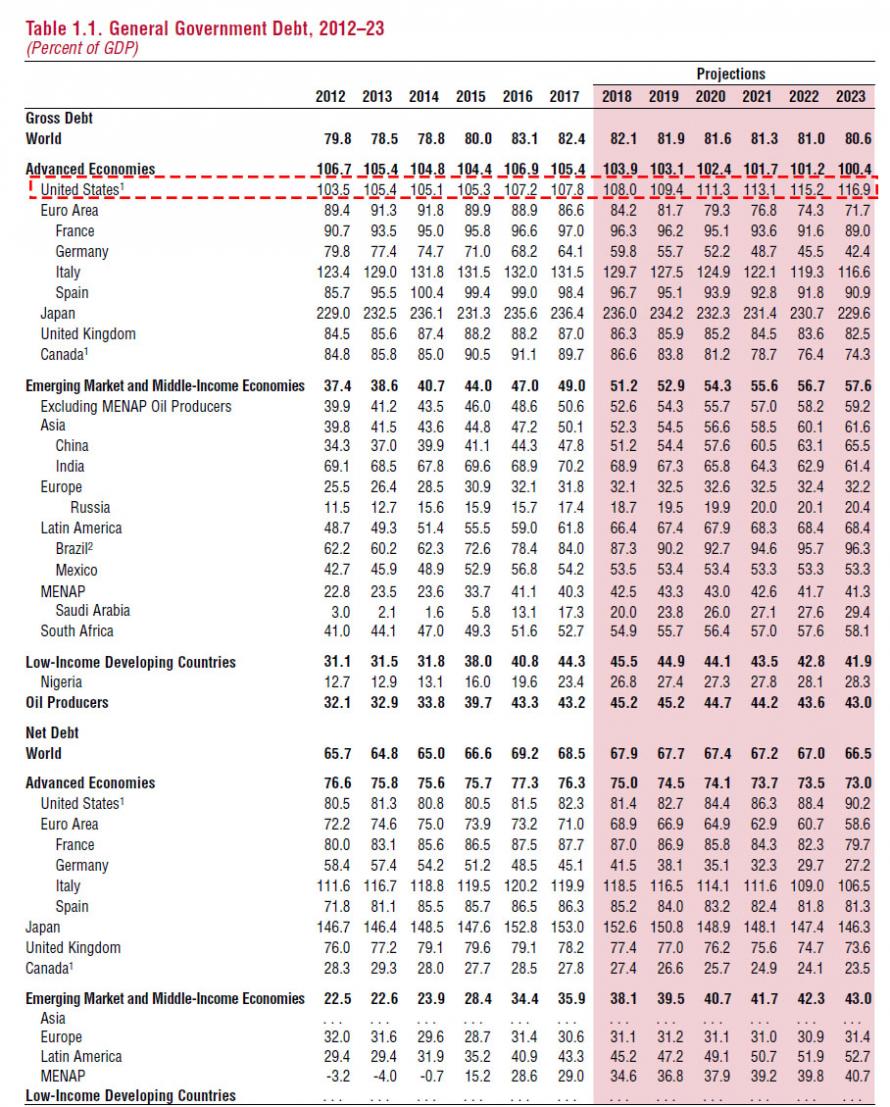

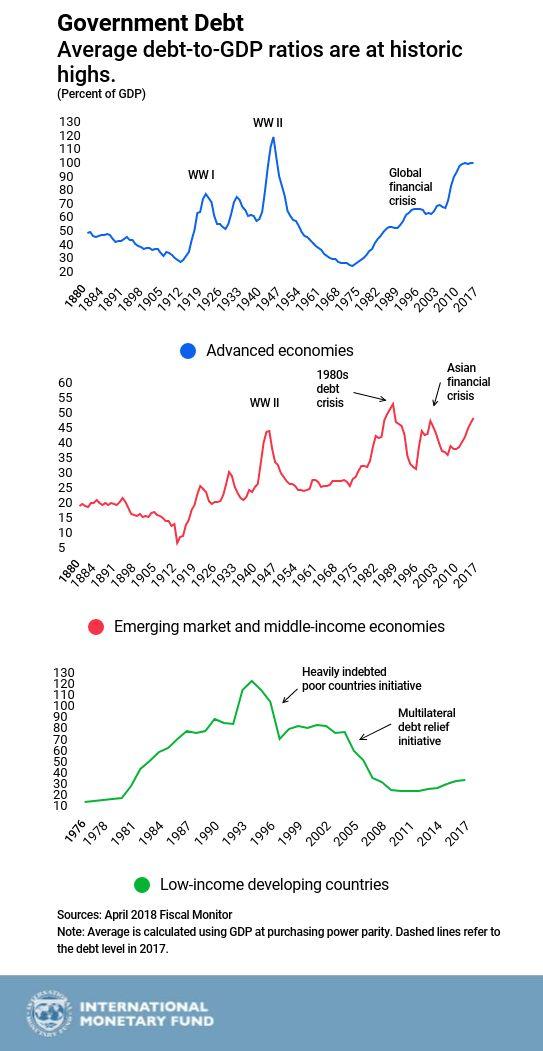

Fast forward exactly one year to today, when the IMF once again sounded the alarm on debt, only this time on the public side of the ledger, warning about – what else – excessive global borrowing, and noting that with a total of $164 trillion of debt, or 225% of global debt to GDP…

… the world’s public and private sectors are more in debt now than at the peak of the 2008 financial crisis, when global debt/GDP peaked at 213%.

Some more details from the IMF: while advanced economies are responsible for most global debt, in the last ten years, emerging market economies have been responsible for most of the increase. In fact, as we showed several months ago, China alone contributed 43% to the increase in total global debt since 2007. In contrast, the contribution from low income developing countries is barely noticeable.

When looking at the big picture, needless to say, it’s all about the US, China, and Japan: these three countries alone accounted for half of the $164tr total in global public and private sector debt. And speaking again of China, its debt surged from $1.7 trillion in 2001 to $25.5 trillion in 2016, and was described by the IMF as the “driving force” behind the increase in global debts, accounting for three-quarters of the rise in private sector debt in the past decade.

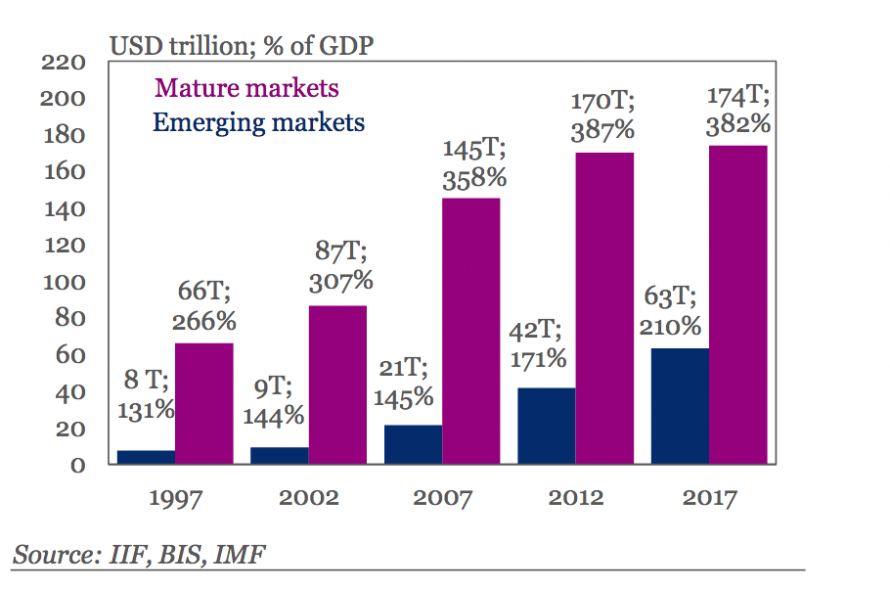

Here we should note that the IMF’s definition of debt is clearly different from that of the Institute of International Finance (IIF), which last week calculated that global debt had hit $237 trillion in debt or 318% debt/GDP.

Whatever the differences in debt calculating methodology, both agencies can agree on one thing: debt has never been greater and it once again poses an existential threat to the so-called “coordinated recovery”, which of course, only exists thanks to said surge in global debt.

Leave A Comment