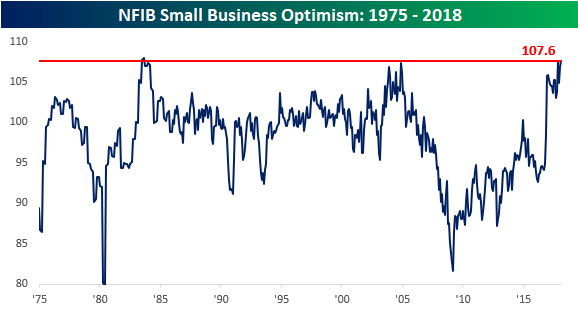

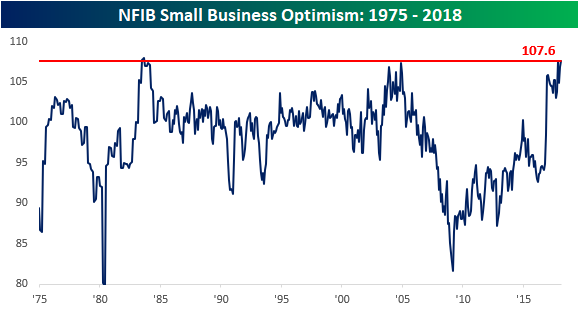

Say what you want about the pace of economic growth, but most small business owners are downright giddy and the most confident they have been in their careers. The latest evidence is the monthly sentiment survey of small businesses from the NFIB. In this month’s report, the headline index came in higher than expected, rising from 106.9 to 107.6 versus expectations for an increase to 107.1. The last time the index was this high was in September 1983, and in the history of the survey, the index has only been higher twice. Check out the long-term chart below. In 1983, there were two months where the index exceeded this month’s reading, and in 2004 it got close to current levels but came up just short.

From a shorter-term perspective, this month’s increase to new multi-decade highs continues the surge that began in November 2016 and puts the current reading a full ten percentage points above its historical average dating back to 2000.

When President Trump campaigned, he ran on a platform of reducing the regulatory and tax burden for American businesses. Based on the trends we have seen from the monthly Small Business Optimism report since he was elected, his actions have certainly had an impact. Take the “most important problem” question in each month’s report. Back in October 2016, before President Trump was elected, a combined 42% of small businesses cited either Taxes or Government Regulation as their biggest problem, and the two were tied for the lead as being cited by the largest percentage of businesses. In the most recent report, the combined reading of these two problems is just 30%, which is the lowest in eight years!

The table below lists the percentage of small businesses that cited each of the problems below as their most important problem. This month, Quality of Labor leads the list at 22%, while Taxes and Red Tape are tied at 15%. The labor quality issue has been a concern for the market since it might have an inflationary impact as employers are forced to pay up for higher quality workers. This month, though, both “Quality of Labor” and “Cost of Labor” were flat month-over-month, which should soothe the market a bit.

Leave A Comment