No one knows if yesterday’s 3%-plus plunge in US equity prices is noise or the start of an extended decline. What we do know is that the slide wasn’t entirely unexpected given the strong relative and absolute performance of US stocks in recent history.

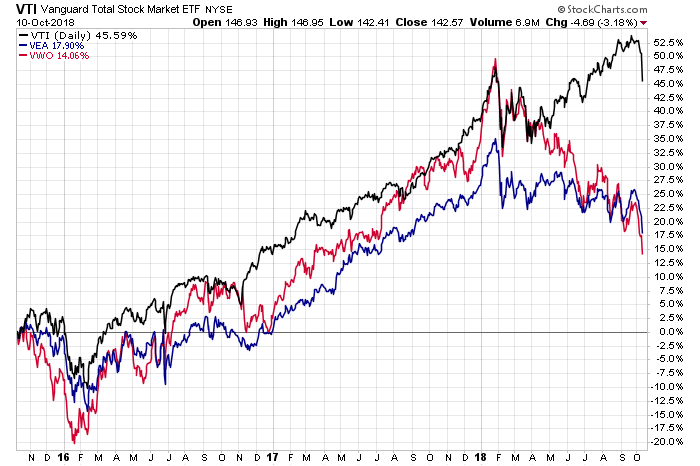

As noted in Monday’s review of global markets through an ETF lens, equities in the US have been on a tear lately. As of last week’s close, Vanguard Total Stock Market (VTI) was up more than 14% for the past year vs. a roughly flat performance for foreign stocks in developed markets (Vanguard FTSE Developed Markets ETF (VEA)) and a roughly 10% loss for emerging-markets equities (Vanguard FTSE Emerging Markets ETF (VWO)), as of Oct. 5.

Longer-run windows also show a dramatic edge for US equities. For the trailing three-year window, for instance, VTI is still up sharply (annualized 11.1% return) vs. VEA and VWO (+2.6% and +1.9%, respective), even after yesterday’s rout.

The divergence in favor of the US market has been particularly striking since March. While foreign equities have been trending down for months, US stocks have been consistently making new highs – a mismatch that’s gone to extremes…until yesterday.

History tells us that while large divergences are possible at times, they’re unsustainable. What was the source of the divergence? Maybe the crowd had assumed that an extraordinary economic boom in the US would carry the day. Whatever the explanation, a huge gap unfolded in performance between the US and the rest of world – a gap that was destined to close at some point.

“The sharp rise in US 10-year yields has caused investors to suddenly reprice the impact of moving from post-crisis low yields to a rising rate environment,”advises Eleanor Creagh, a strategist at Saxo Capital Markets in Sydney. “We have the global growth engines, price of energy rising, price of money rising and quantity of money falling combined with the ongoing trend of de-globalization which has started to impact markets and the cracks are showing.”

Leave A Comment