Oclaro (OCLR) was originally selected as a Long Idea on 1/17/18. At the time of the report, the stock received a Very Attractive rating. Our investment thesis highlighted dramatic economic earnings growth, a significant technological advantage, overstated concerns about China, and a valuation that implied a permanent 30% decline in after-tax profit (NOPAT). We added the stock to our Focus List on 1/18/18.

We kept the position open for a few weeks in the hopes that FNSR might come in with a higher bid, but enough time has elapsed that this no longer seems likely, so we are closing our OCLR position.

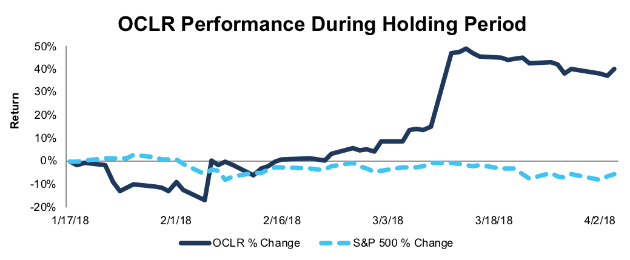

Oclaro outperformed as a long idea over the 77-day holding period, gaining 39% while the S&P fell by 6%.

Figure 1: OCLR vs. S&P 500 – Price Return

Sources: New Constructs, LLC and company filings

Note: Gain/Decline performance analysis excludes transaction costs and dividends.

We think this acquisition is a good deal for LITE. Based on OCLR’s current NOPAT, LITE will earn a return on invested capital (ROIC) of 7.4% on the acquisition, which is greater than its weighted average cost of capital (WACC) of 5.6%. Despite its strong fundamentals, LITE’s expensive valuation means it only earns a Neutral Risk/Reward rating.

Leave A Comment