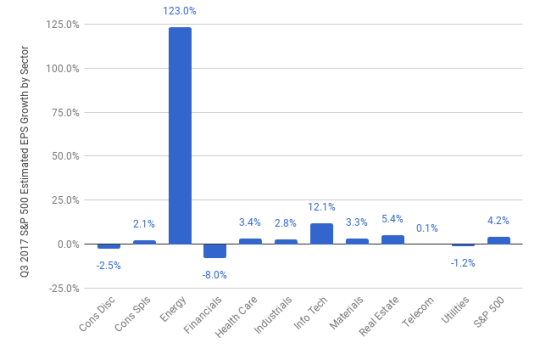

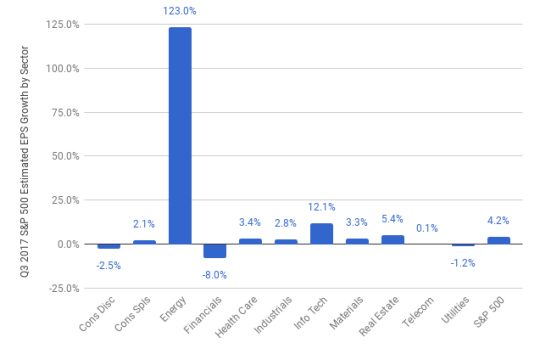

The big banks kicked off earnings season on a fairly high note when they reported last week, with JPMorgan and Bank of America beating on both the top and the bottom line, Citi only beating on the top line, while Wells Fargo missed on both. Overall the Estimize community is expecting another strong earnings season, but a pull back from the first half of the year. S&P 500 EPS is anticipated to grow 4.2% from the year ago quarter, a deceleration from last quarter’s 10.2%. Revenues are expected to grow 6%, up slightly from 5.2% in Q2.

In a near repeat of last quarter, winning sectors once again include Energy and Technology, while Consumer Discretionary remains as one of the biggest laggards, only to be topped by Financials.

Energy is leading the pack right now with expected growth of almost 123% due to easier year-over-year comparisons. If you remove energy, index growth is almost cut in half to 2.5%, just shy of the 20 year historical average. The question then becomes, is 2.5% growth enough to justify a market that is trading at nearly 19x? Investors may be wishing for stronger fundamentals at these prices.

Following energy, technology is expected to see the second highest growth rate of all the sectors with profit growth of 12.1% and revenue growth of 8%. All 10 industries within the sector are estimated to record positive numbers this quarter, but none more than semiconductors which are currently anticipated to increase earnings by 50% YoY. Micron Technology is driving the semiconductors and is the largest contributor to sector growth. The company posted EPS of $2.02 on September 26, a record high, vs. the year ago result of -$0.05, an increase of 4140%. Optimism around Micron’s stock is due to favorable pricing of DRAM and NAND chips, MU’s main businesses. Next week we’ll hear from more big names in this space, including Advanced Micro Devices, Texas Instruments, and Intel, among others.

Leave A Comment