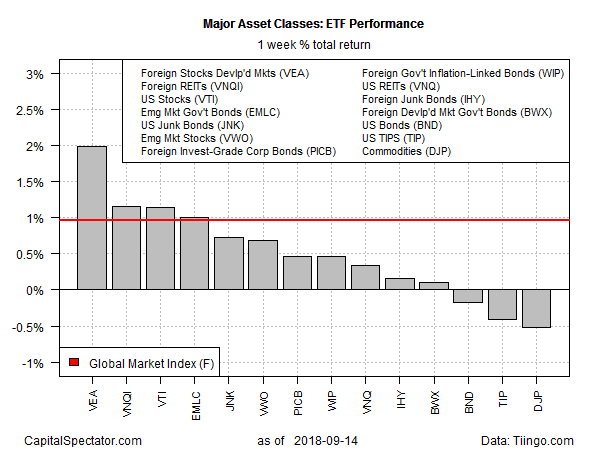

US and foreign stock markets firmed up last week, including the recently pummeled slice of emerging-markets equities, based on a set of exchange-traded products. Meanwhile, US investment-grade bonds and broadly defined commodities posted the only setbacks for the major asset classes over the five trading days through Sep. 14.

Foreign stocks in developed markets jumped the most last week. Vanguard FTSE Developed Markets (VEA) gained 2.0%. Note, however, that the ETF has been trending lower for most of this year and it’s unclear if downside bias has run its course.

Stocks in emerging markets also edged up last week. Vanguard FTSE Emerging Markets (VWO) added 0.7%, its first weekly advance in nearly a month. This year’s downward trend, however, still appears to be intact via VWO too.

News that China’s stock market on Monday fell to its lowest level in nearly four years on renewed fears of an escalating trade war with the US suggests that emerging-markets equities could still be headed for more weakness.

Nonetheless, one analyst thinks a bottom for assets in emerging markets may be near. Bloomberg earlier today reported: “Franklin Templeton Investments says the rout in emerging markets may be nearing a bottom though reckons there are still countries like the Philippines that will suffer.”

The general upswing in most assets last week lifted an ETF-based version of the Global Markets Index (GMI.F). This investable, unmanaged benchmark that holds all the major asset classes in market-value weights gained roughly 1.0% last week — its best weekly increase in three weeks.

Turning to one-year results, US stocks continue to dominate the winner’s list by a wide margin. Vanguard Total Stock Market (VTI) is currently up by 19.2% in total-return terms. The rest of the major asset classes are far behind.

Indeed, the second-best performer at the moment: SPDR Bloomberg Barclays High Yield Bond (JNK) is up a modest 2.3% after factoring in distributions for the trailing one-year window.

Leave A Comment