Earlier we reminded readers about the circular (and why note fraudulent conveyance) scheme hatched by JPMorgan to reduce its secured loan exposure to Weatherford, when just two weeks ago none other than JPM underwrote an WFT equity offering in which it sold equity in the company, and which proceeds were promptly used by the company to repay the JPMorgan revolver.

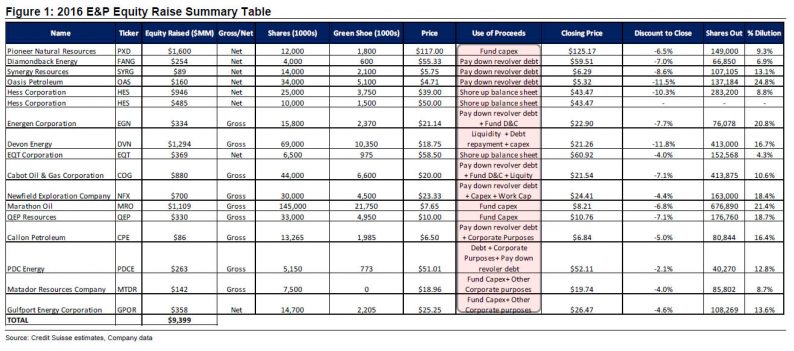

We then showed that it wasn’t just Weatherford: most of the “uses of funds” from the recent record surge in oil and gas equity offerings, have been used to repay the secured debt/revolver facilities, thereby eliminating funded and unfunded balance sheet exposure of major US banks.

But while lender banks are all too eager to take advantage of the brief surge in equity prices just so they can “help” their clients dilute their shareholder base so to repay the very same lender banks, they know quite well that the equity offering window is rapidly closing; in fact it will slam shut as soon as the price of oil resumes its downward trajectory.

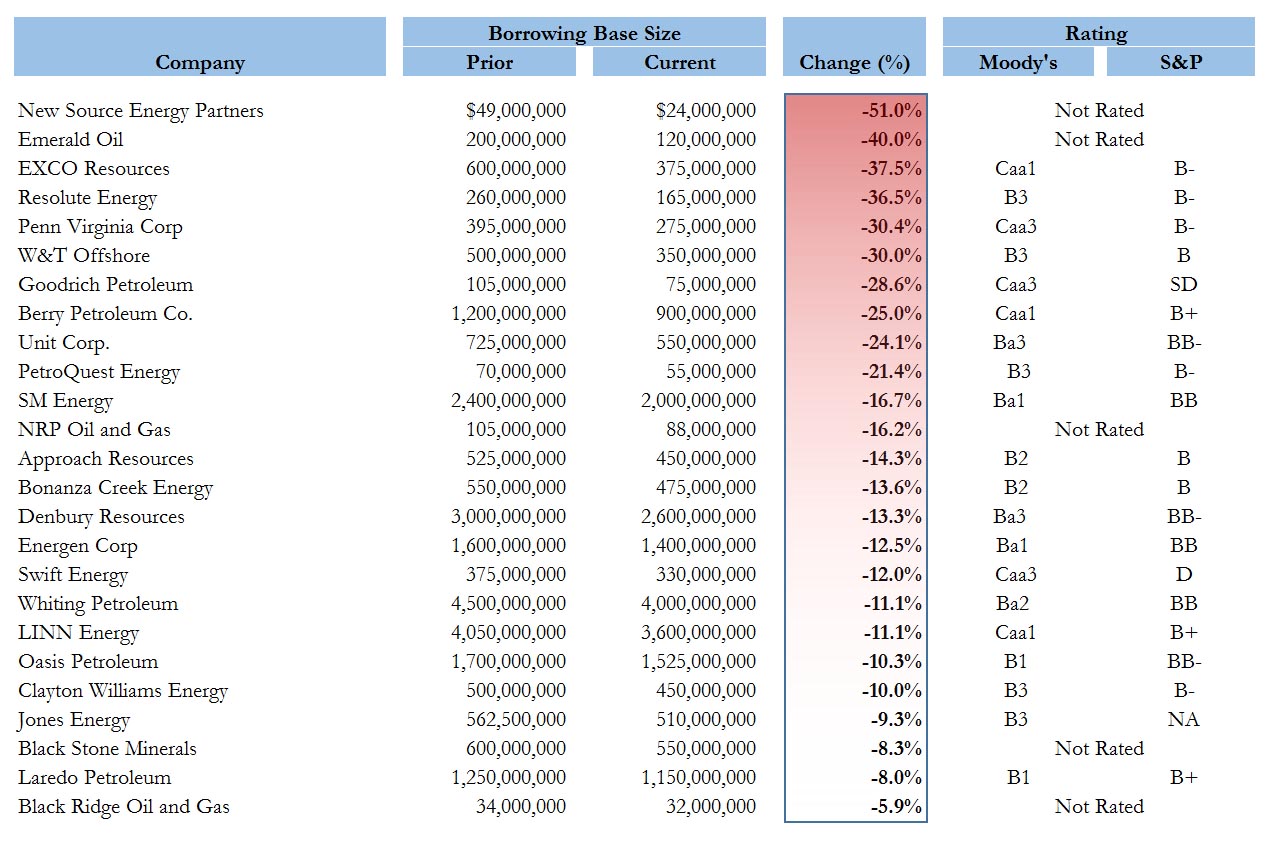

That does not mean they are out of options to reduce their exposure to US shale, however. Quite the contrary, and in fact the “exposure reduction” is about to begin in earnest. We hinted at what it would look like in early January when we reported that already some 25 of the most distressed shale companies have seen their revolving bases slashed by as much as 50%.

These were just the beginning. As Bloomberg wrote earlier, U.S. exploration and production companies must brace for further cuts to their borrowing-base credit lines this spring, as part of the spring 2016 borrowing base redeterminations.

According to Bloomberg, Royal Bank of Canada estimated that cuts to U.S. borrowing-base credit lines last fall averaged only 6%, while – ironically enough – JPMorgan predicts that the average cut may reach 20% over the next several months. JPMorgan expects some credit lines to be chopped by as much as 50%.

Leave A Comment