Under pressure from investors, Glencore Plc (GLNCY), the world’s largest corporate player in the commodities market, recently announced a plan to slash as much as $10.2B in debt by offering additional shares to the market, selling assets, and eliminating dividends.In the first half of 2015, Glencore spent $1.8B on distributions and buybacks,

Glencore reassured investors that this plan will not impact core business activities.

I take three primary lessons or implications from this move by mighty Glencore:

From point #1 and #2, I have slowed down my eagerness to shop for additional cheap commodity plays. Some commodity plays are likely still good shorts on rallies. Point #3 means that the upside risk (opportunity) for RIO has significantly come down. I no longer view my long-term call options on RIO as a hedge/lottery ticket on a potential deal with Glencore. There goes the Rio Tinto “exit strategy.”

Source: FreeStockCharts.com

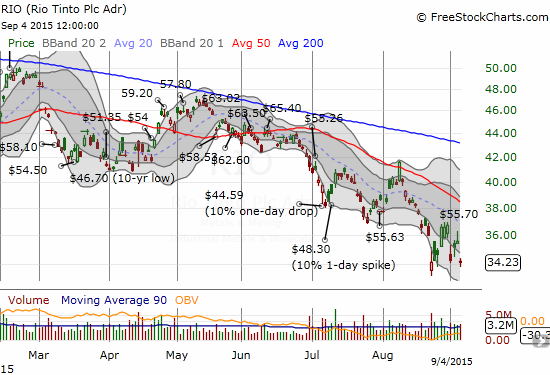

In recent trade, Rio Tinto (RIO) has bounced around largely independent from the volatility in the price of iron ore (shown approximately as an overlay). While I still do not want to short RIO, shorts of BHP Billiton Limited (BHP) are quite sufficient for taking the bearish side of the iron ore trade. Like so many commodity-related stocks, BHP is firmly locked within a well-defined downtrend.

Leave A Comment