Yesterday’s Japan flash-crash inspired selling continues for a second day, with global equities – and bonds – sliding early Friday on concerns U.S. tax reform – and corporate tax cuts – will be delayed after Senate Republicans unveiled a plan that differed significantly from the House of Representatives’ version. After suffering their biggest plunge in 4 months on Thursday, European stocks failed to find a bid along with Asian stocks, while U.S. index futures pointed to a lower open (ES -0.5%, or -10), the Nikkei 225 ended 0.8% lower, Treasuries fell as did the Bloomberg Dollar Spot Index, which declined for a third day.

And here is one for the streak watchers: on Thursday the global MSCI index failed by one day to post its longest winning streak since 2003 as it fell 0.4% following 10 days straight of gains. The MSCI world index gained more than 18% so far this year and some investors believe a pullback is due. “I think there’s a feeling out there that there’s a long awaited correction, and no one wants to be caught by surprise,” said Emmanuel Cau, global equity strategist at JP Morgan.“When the market is down a bit people tend to extrapolate. But I think it’s simply a bit of profit taking and digesting from a very strong September and October.”

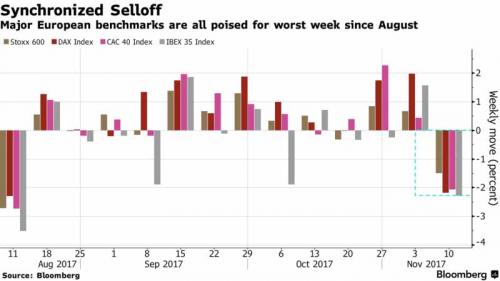

Europe’s benchmark Stoxx 600 reversed an early rebound, falling 0.2% on high volume;It is on track for its worst week in three months, if it falls on Friday , its fourth drop in row. Carmakers and retailers led the index to its biggest two-day drop since August as third-quarter earnings season continues, with aerospace-electronics maker Leonardo SpA crashing 20% after cutting sales forecasts.

In Asia it was more of the same, with stocks declining after a rally that saw them touch a record high less than 48 hours earlier, as shares in Japan extended losses following abrupt swings on Thursday. Asian stocks fell, tracking weakness in U.S. equities after the U.S. Senate released a tax plan that would delay cuts to the corporate rate until 2019, defying President Donald Trump. The MSCI Asia Pacific Index dropped 0.4 percent to 171.18, trimming its weekly advance to 0.8%; The MSCI Asia Pacific ex-Japan index fell 0.3%, while Japan’s Nikkei lost 0.8%, slipping off Thursday’s 21-year high after a 16% rally in the past two months. The decline was led by Japanese equities, which extended a loss Thursday on the heels of the largest one-day swing in a year. The Asian benchmark gauge has risen for six straight weeks, posting gains in 16 of the past 18 weeks. Thursday’s close was less than half a point from a record.

“Investors are unwinding expectations on Trump’s ambitious tax reform,” Margaret Yang, a Singapore-based strategist at CMC, said by phone. “Delay in tax cuts is the perfect excuse to book profits, but long-term fundamentals remain positive for Asian equities.” While most Asian markets fell, Hong Kong stocks traded higher, and Shanghai’s benchmark index headed for its best week since August, led by brokerages.

Meanwhile, in a move that smacks of a risk-parity deleveraging unwind, instead of dipping – as a risk-haven – 10Y TSY yields rose a third day, and core European bond yields followed suit (not to mention the rout in ongoing junk bonds). Indeed, as the Stoxx 600 dropped, Germany leads the bond market lower, sending 10-year Bund yield to a two-week high. Treasuries decline in tandem with the long-end underperforming and finally steepening the 5s30s curve from the narrowest level in a decade.

“The world looks, if anything, more frightening given declines in both bonds and stocks,” Ole Hansen, head of commodity strategy at Saxo Bank A/S in Hellerup, Denmark, said by email. “Higher lows and lower highs following the U.S. presidential election a year ago shows a market in need of a proper spark. So far that spark remains illusive.”

In macro, majors FX pairs were trapped in familiar ranges, while bonds stole the spotlight yet again as yields ticked up steadily across traders’ screens; the Bloomberg Dollar Spot Index attempted a feeble recovery after short-term accounts took profit on shorts, but the gains lacked conviction; the pound flapped about, seeking a decisive direction, ahead of a key Brexit briefing; Treasury 10-year yields were inching closer toward the key 2.40% level. WTI crude was steady above $57 a barrel.

The catalyst for the move was yesterday’s tax reform fireworks, where Republican senators said they wanted to slash the corporate tax rate in 2019, later than the House’s proposed schedule of 2018, complicating a push for the biggest overhaul of U.S. tax law since the 1980s. The House was set to vote on its measure next week. But the Senate’s timetable was less clear.

“Things look fluid, including on when the tax cut deal will be reached,” said Hirokazu Kabeya, chief global strategist at Daiwa Securities.“I would say a compromise will be reached …But if they indeed decide to delay the tax cut by a year, there is likely to be some disappointment.”

In FX, the euro declined 0.1% to 1.1641, while sterling was 0.1% higherat 1.3162.

In rates, the 10y TSY rose to 2.3753% , while Bund yields, as noted above, climbed to their highest level in over a week as euro zone bonds sold off across the board for a second consecutive day. The yield on Germany’s 10-year bund hit 0.40% for the first time since Oct. 27.

Among commodities, oil prices steadied on expectations of supply cuts by major exporters as well as continuing concern about political developments in Saudi Arabia. A spokesman for Saudi Arabia’s energy ministry said the kingdom planned to cut crude exports by 120,000 barrels per day in December from November. Brent crude was at $64.01 per barrel, close to the 2-year high of $64.65 reached earlier this week. WTI traded at $57.17, also just shy of this week’s more than two-year high of $57.69. Concerns about the stability of Saudi Arabia, sparked after the purge of 11 princes and arrests of dozen other influential figures since last week, are intensifying. Sources told Reuters that Lebanon believes the country’s former prime minister, Saad al-Hariri, was being held in Saudi Arabia, although Saudi Arabia denied reports he was under house arrest. Saudi Arabia accused Beirut earlier this week of declaring war against the kingdom.

Leave A Comment