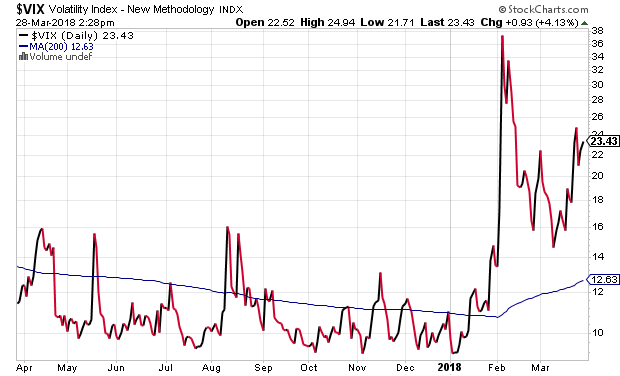

According to Bank of America’s research team, 87% of prior bull-to-bear transitions involved increases in volatility. That’s not particularly surprising. Anyone who has experienced a stock bear probably remembers months and months of extraordinary price swings.

In the current bull portion of the bull-bear cycle (3/09-?), each of the previous corrections offered buying opportunities. For example, there were two 10%-plus volatile price pullbacks during the earnings recession (2015-2016). Earnings per share across the S&P 500 kept shrinking, yet buying the August 2015 dip and the January 2016 sell-off proved beneficial. Similarly, in the 2nd quarter of 2012, the S&P 500 sank into correction mode due to domestic employment concerns and fears of Euro-zone economic contraction. Nevertheless, shrugging off the global economic worries and acquiring more stock ultimately benefited risk-takers.

The 2011 sovereign debt crisis may have been more difficult with regard to “keeping the faith.” European stocks shed 40% whereas the S&P 500 managed to survive with a 19% top-to-bottom decline. Yet, those that believed Portugal, Italy, Greece and Spain (PIGS) would find a path for holding it together were richly rewarded.

What many fail to recognize about these previous corrective phases, as opposed to 2018’s unresolved pullback, is the extent of central bank accommodation that had been enacted. In 2011, Eurozone members established the European Financial Stability Facility, providing emergency lending to troubled nations. That was not enough. The head of the European Central Bank (ECB) Mario Draghi made good on his words to do “whatever it takes” to preserve the euro-zone. It followed that the ECB bought gobs of junk-rated sovereign bonds, pushing borrowing costs into the basement so that nations could pay back the interest on their excessive debt loads.

In 2012, as the U.S. stock market was rolling over, the Federal Reserve (Fed) unleashed its most ambitious electronic money creating scheme yet: Open-ended QE3. The Fed bought hundreds upon hundreds of billions in government obligations with currency credits created out of thin air, pushing borrowing costs ever-downward to stimulate the U.S. economy.

Leave A Comment