We’re always trying to build a better mousetrap around here by adding non-correlated asset classes to our portfolio. While there is no “free lunch” in economics, true diversification is about as close as you’re ever going to get. And by “true diversification,” I mean adding assets to the portfolio that really do zig when the others zag. A portfolio of 100 stocks doesn’t offer much diversification benefit when the entire market rolls over.

At any rate, Dr. Phillip Guerra and I have cooked up a suite of alternative portfolios based on the principles of risk parity. We’ve been running our Active Risk Parity Portfolio With 7% Annual Volatility Target live since September, and we’ve backtested it to 1996.

The results aren’t too shabby, if I do say so myself. Average annual returns of 11.5% with a maximum drawdown of just 9.8% and a correlation to the stock market of just 0.24.

Rather than target returns — which are impossible to know with any accuracy in advance — we target volatility. While volatility will also fluctuate over time, we find it to be more accurate to target and also that it gives us a better handle on risk. The key to making money over time is first to avoid losing it.

I don’t consider this a replacement for a traditional long stock portfolio. In fact, most of the money I manage is long-only and dividend focused. But I certainly do consider this a nice addition to a traditional stock portfolio. With bonds not likely to offer much in the way of return any time soon, you need viable alternatives for the “40” in the old 60/40 portfolio of stocks and bonds. A risk parity model can certainly fill that role.

For more information on alternative portfolios in general, see here.

Related Posts

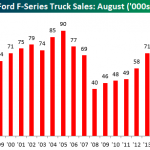

Ford Truck Sales – No Slowdown Here

Ford Truck Sales – No Slowdown Here “Davidson” On Inflation And Pessimism

“Davidson” On Inflation And Pessimism Is This The Long-Awaited Silver Short Squeeze, The Beginning Of The Next Bull Market, Or Both? Or, Sigh, Neither?

Is This The Long-Awaited Silver Short Squeeze, The Beginning Of The Next Bull Market, Or Both? Or, Sigh, Neither? S&P 500 And Nasdaq 100 Forecast – Thursday, Oct. 4

S&P 500 And Nasdaq 100 Forecast – Thursday, Oct. 4 Ethereum Prices Search For Support As Adoption Doubts Intensify

Ethereum Prices Search For Support As Adoption Doubts Intensify- Index Funds Vs. Hedge Funds: Buffett’s Bet, 10 Years Later

Leave A Comment