Some influences on the stock market are casual, subtle or open to interpretation, but the catalyst behind the current stock market rally really shouldn’t be controversial. As far as stocks go, we have lived by QE. The only question now is, whether we will die without it.

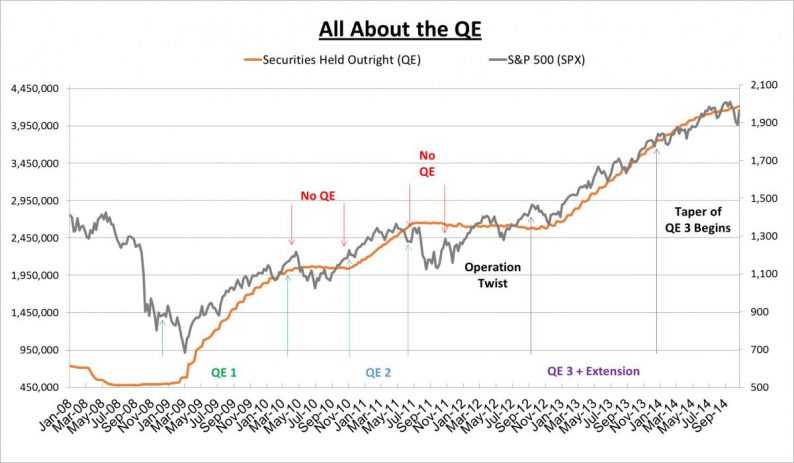

Since the financial crisis of 2008 stock prices have only risen when the Fed is either expanding its balance sheet, hinting that it is about to do so, or actively recycling assets to hold down long term interest rates. Absent any of these aggressive moves, stocks have shown a clear tendency to fall. Curiously, while most investors now believe that QE is in the past, few would argue that the bull market is in danger. But a quick look at how much influence the Fed’s operations have had on market performance should send a chill down Wall Street. The Chart below should speak for itself:

Created by EPC using data from the Federal Reserve and Bloomberg

When the markets crashed in the fall of 2008, the Fed announced QE1, a plan to purchase $600 billion in mortgage-backed securities (MBS) and agency debt, which was later expanded in March 2009 by another $750 billion. QE1 expanded the Fed’s balance by 247%, to $1.43 trillion. Over that time, the S&P 500 put in a rally of 71%.

But from April to November 2010, with QE on hiatus and the Fed’s balance sheet hardly expanding, stocks declined by about 11%. But when Fed Chairman Ben Bernanke strongly hinted in August 2010 that the Fed was ready to launch another round of QE, the markets rallied 18% in five months. By the time QE2 ran its course, the Fed’ balance sheet had swelled by 29.4%, and the S&P 500 had rallied about 25%.

But when the curtain came down on QE2, and Wall Street had no hints that an encore was imminent, the S&P 500 put in a wicked 16% sell-off between July and August 19. So on September 21, 2011, Bernanke announced the implementation of “Operation Twist,” authorizing the purchase of $400 billion of long term Treasury bonds financed by the sales of shorter term bonds, thereby extending the average maturity of the Fed’s portfolio and lowering long term interest rates. It was hoped that Twist would offer the benefits of QE without expanding the Fed’s balance sheet.

Related Posts

Geopolitical Risk, “Fear Cycle” Driving Oil Prices Higher

Geopolitical Risk, “Fear Cycle” Driving Oil Prices Higher E

Why Sarepta Therapeutics Inc Looks On Track For A Second DMD Approval

E

Why Sarepta Therapeutics Inc Looks On Track For A Second DMD Approval Northwest Biotherapeutics: Why The Phase 3 Trial Of DCVax-L In Newly Diagnosed Glioblastoma Patients Has A Good Chance For Success

Northwest Biotherapeutics: Why The Phase 3 Trial Of DCVax-L In Newly Diagnosed Glioblastoma Patients Has A Good Chance For Success Day Trading Stock Picks For This Week – Tuesday, April 25

Day Trading Stock Picks For This Week – Tuesday, April 25 GBP/USD And British Pound Futures Seasonality – Best Times Of Year To Buy And Sell

GBP/USD And British Pound Futures Seasonality – Best Times Of Year To Buy And Sell Yellen, Employment & Policy Errors

Yellen, Employment & Policy Errors

Leave A Comment