Inflation! Deflation!

Two words that strike fear into the hearts of investors.

Are such fears justified? Let’s take a look…

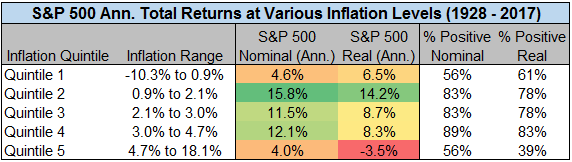

If we segment calendar year changes in the Consumer Price Index (CPI) into quintiles, we observe the following:

Source Data for all tables herein: YCharts, BLS, Stern.NYU.edu/~adamodar

During years with the highest inflation (quintile 5):

During years with the lowest inflation (quintile 1):

What’s left? The so-called “goldilocks” periods in which inflation was running neither too cold nor too hot (in a range between 1.2% and 4.7%). It was during these quintiles that stocks posted their best returns on both a nominal and real basis.

Related Posts

New York Is The 9th Most Expensive City In The World – Singapore Ranks No.1

New York Is The 9th Most Expensive City In The World – Singapore Ranks No.1- U.K. Services Sector Slows In April; Pound Dips

ECRI Weekly Leading Index Update

ECRI Weekly Leading Index Update S&P 500 Adam And Adam Double Bottom Pattern In Progress

S&P 500 Adam And Adam Double Bottom Pattern In Progress Did President Obama Seal The ‘No’ Vote On The Renzi Referendum?

Did President Obama Seal The ‘No’ Vote On The Renzi Referendum? BTC/USD And BTC/JPY Forecast – Tuesday, April 3

BTC/USD And BTC/JPY Forecast – Tuesday, April 3

Leave A Comment