Successful investors live by a golden rule: what the mainstream financial media talks about is not important. They focus on what they don’t hear instead. So forget about Yellen for a second. Let go of Draghi, oil, the South African rand and Syria. That’s all in the now. But investing is about the future.

We are convinced there is one proverbial elephant in the room in particular that will shape our future. And that elephant is Japan. The ‘widowmaker’ trade has been claiming financial lives for multiple decades now. That is, short JGBs, or Japanese Government Bonds, was so obvious a trade that it never worked. The 10-year yield currently trades at 0,31%, which is close to the all-time low. We’re still waiting for the shoe to drop.

Will it ever drop? We believe it will. ‘Drop’ might not be the appropriate word. The accumulation of imbalances might trigger a cascade of events that will shake the world at its core. Let’s investigate some data.

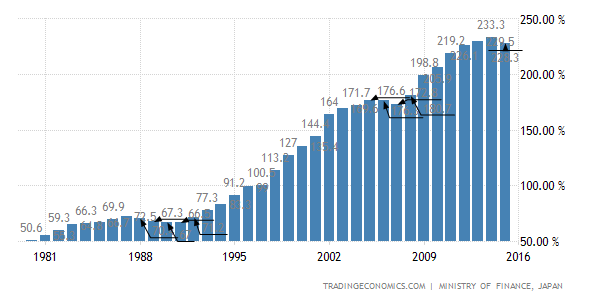

Japan’s debt-to-GDP ratio has hit a unprecedented 230%. You probably knew that. But it doesn’t keep you awake at night. We are genetically wired to focus on acute danger. If a tiger approaches us, we focus. But if stands still and doesn’t move for years, we turn around in search for other dangers. Wise investors remind themselves constantly of the tiger though. They never let their guard down.

What about the pace at which debt-to-GDP is ramping up? The budget deficit tells us all we need to know.

For six years in a row already, Japan scored around minus 8%. And given the flattish GDP, these annual percentages head straight to the public debt pile. Japan’s long term potential real GDP-growth rate is simply close to zero, given the demographics. The latest quarterly print was a minus 0.3%. This makes the debt grow even faster.

The GDP leads us to the approach that governments used time and again in history to reduce debt loads: nominal GDP-targeting. Also known as inflation-targeting, financial repression, money printing, and monetary stimulus. The Bank of Japan (BoJ) is working hard in that respect. It already owns over 30% of the total JGB market. In a few years, Japan Macro Advisors (JMA) projects the BoJ might be holding over 60% of the total market given its current policies.

Related Posts

Morning Call For Tuesday, Dec. 19

Morning Call For Tuesday, Dec. 19- Telecom Stock Roundup: Solid Q4 For ATUS, TDS, USM, WIN And FTR, Mixed Bag For AMT

- E

Celldex Announces Discontinuation Of Phase 3 Trial In Patients With Brain Cancer

Understand Your Liabilities

Understand Your Liabilities- Lose Lose Lose Affair: Farm Lobby Turns Up Heat On Trump Over NAFTA

Avis Budget Q4 Earnings Beat Estimates, ’18 View Solid

Avis Budget Q4 Earnings Beat Estimates, ’18 View Solid

Leave A Comment