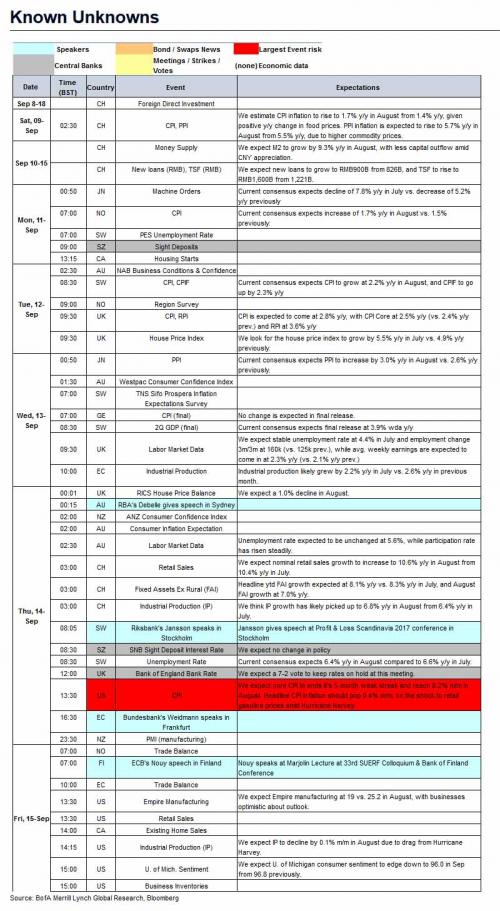

In a somewhat quieter week for economic news, this week’s focus is on BoE and SNB policy meetings as well as on inflation releases in US, UK, China and others. Other releases of note include retail sales in the US, UK and China along with industrial production in US, Eurozone & China.

Key events:

As BofA previews the week’s main events, watch for BoE and SNB meetings:

After a surprise hike from the BoC last week, we turn the attention to the BoE and SNB. At the BoE meeting on Thursday, consensus expects a 7-2 vote to leave rates unchanged. This said, given the GBP depreciation since the August meeting, the rhetoric will be less dovish and with the potential to challenge current rate hike pricing upwards. Again, the relevance of such rhetoric is purely confined to market communication: no rate hike is expected before 2019.

Also the SNB holds the monetary policy meeting on Thursday: our economists do not expect a policy change. The economic rationale for very accommodative policy remains. In fact, GDP growth has been disappointing and nominal wage dynamics remain subdued while the ECB has not meaningfully changed its policy stance, yet.

…and inflation releases in the US, UK and others

Economists expect US inflation to increase to 0.2% m/m, while headline inflation is set to rise to 0.4%, given Hurricane Harvey’s impact on gasoline prices. UK inflation is expected to come in somewhat hot at 0.5% m/m.

A detailed breakdown of key events by day, courtesy of Deutsche Bank:

Related Posts

The Puzzling Weakness In U.S. Companies’ Capital Spending

The Puzzling Weakness In U.S. Companies’ Capital Spending A New Year For China: Monkey Business

A New Year For China: Monkey Business What bear market? These crypto websites see traffic rising in 2023

What bear market? These crypto websites see traffic rising in 2023 $4.5T asset manager Fidelity offers ETH custody and trading to clients

$4.5T asset manager Fidelity offers ETH custody and trading to clients Spotify Raises $1 Billion In Debt

Spotify Raises $1 Billion In Debt September 2018: ECRI’s WLI Growth Rate Index Improvement Continues But Still Shows Insignificant Growth

September 2018: ECRI’s WLI Growth Rate Index Improvement Continues But Still Shows Insignificant Growth

Leave A Comment