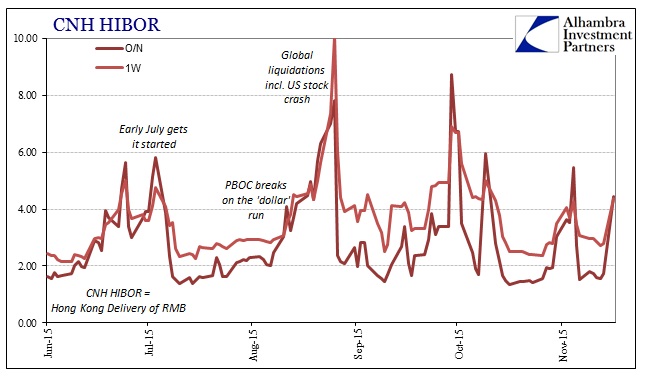

The overnight rate in offshore renminbi liquidity surged over 4% today, the fifth such notable heave in this half of 2015. The rate had been under 2% for the six trading days before and including Friday, but overnight CNH HIBOR jumped from 1.7325% to 4.4525% over the weekend. The one-week maturity similarly spiked, moving from 2.796% at the end of last week to 4.3705% to start this one. Even the 3-month CNH rate, which is typically far, far more stable, increased by more than 60 bps to 4.257%.

Such dramatic moves have become more commonplace in Hong Kong trading of late, coinciding with the obvious travails of eurodollar function especially going back to the start of Q3 (July 6). In more recent weeks, there had been an acute correlation between offshore CNH liquidity and the “price” of “dollar” liquidity in China, as represented by the CNY/USD exchange rate. The PBOC had been involved in pushing that rate upward especially at the end of October after its rate cuts and reserve “release”, but the Chinese central bank has clearly relented on that count. After increasing the country’s official “middle rate” exchange (where the RMB band is anchored), the PBOC has allowed the middle rate to decline for nine straight days includingtoday.

It is, however, interesting to note that the quoted CNY/USD exchange was up in trading this morning when the CNH “fix” was calculated. It might suggest private market function as opposed to strictly artificial imposition by the PBOC’s middle rate, but for whatever case the offshore “tightening” was pronounced – a fact that we can appreciate at least separately from the view of ongoing surliness in UST bills.

As O/N SHIBOR continues to be pinned (pegged) around 1.785%, the exact nature of “dollar” views from China and Hong Kong will be difficult and analysis truly suspect. I think it at least sets up an interesting experiment for the rest of the week, particularly in how the PBOC reacts with its middle rate fixing for tomorrow’s trading: do they continue to allow the band to trade downward (“devaluation”) slightly or will there be a heightened response to the offshore conditions of today?

Related Posts

5 Momentum Stocks To Buy Right Now

5 Momentum Stocks To Buy Right Now Car-tastrophe – GM, Fiat Chrysler Idle 7 Plants; Over 10,000 Workers Affected

Car-tastrophe – GM, Fiat Chrysler Idle 7 Plants; Over 10,000 Workers Affected- Three Ways A Forex Demo Trading Account Can Help You Succeed

Square Rises As Bitcoin Buying Tested On Cash App

Square Rises As Bitcoin Buying Tested On Cash App- US Justice Department on the hunt for DeFi hackers and thieves: Finance Redefined

February CPI – Market Sell Off Or Buy The Dip?

February CPI – Market Sell Off Or Buy The Dip?

Leave A Comment