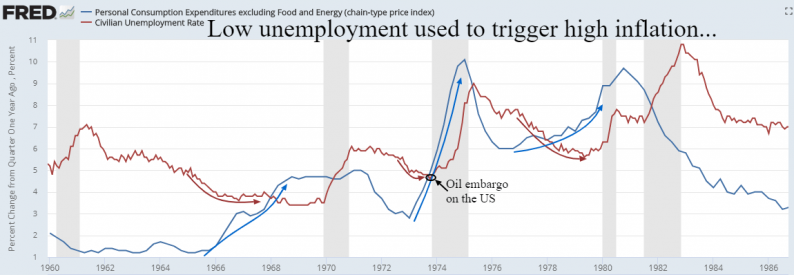

Milton Friedman promulgated the Phillips Curve interpretation that posits a tight labor market generates higher inflation. Since 1967 this has been the primary tool of Central Banks and economists in forecasting inflation. During the previous generation, it appeared that falling unemployment during an economic recovery would always trigger a strong inflation response. Today’s near-record low unemployment should support a robust economic expansion but has confounded economists expecting worrisome inflation. The inflation to unemployment sensitivity was strong in the 1960’s and 1970’s as Boomers entered the workforce triggering abnormal rates of spending and inflation. Combined with the Vietnam War and Johnson’s 1964 War on Poverty, this inflationary Boomer phase caused the US to close the Gold window in 1973 and send the world to free-floating currencies. Pent-up pricing pressures devalued the US Dollar and prompted the infamous Mideast Oil Embargo causing a vicious phase of stagflation until Volker took charge of monetary policy in 1979.

Since Volker’s tight monetary policy of the 1980’s, the unemployment to inflation correlation has been far less acute. The record surge in job seekers in the 1970’s has been replaced by the record surge in job openings today which intuitively should trigger wage inflation. Wages are accelerating at a healthy 3% clip, but higher wages will not create workers that don’t exist.

Record unfilled job openings have boosted job confidence (Quit rate) to 17-year highs, as more workers are willing to quit their job for a better offer. With a very strong GDP and workers trading up for better paychecks inflation is edging higher. Interest rates are rising, not because of inflation fears, but to provide the Fed with ammunition to ease credit when the next recession becomes evident.

Related Posts

The Rally, The Risk, And Realism That Prevails

The Rally, The Risk, And Realism That Prevails Flamingo (FLM) TVL rises as Ethereum gas solutions remain elusive

Flamingo (FLM) TVL rises as Ethereum gas solutions remain elusive FTX seeks sale of Grayscale and Bitwise assets worth $744M

FTX seeks sale of Grayscale and Bitwise assets worth $744M- E

What Glamour Industries Teach Us About Markets

- Price analysis 1/14: BTC, ETH, BNB, SOL, ADA, XRP, LUNA, DOT, AVAX, DOGE

Average Gasoline Prices For Week Ending 10 November 2014 At Lowest Level Since November 2010

Average Gasoline Prices For Week Ending 10 November 2014 At Lowest Level Since November 2010

Leave A Comment