Have we learned anything from Lehman Brothers’ bankruptcy? On Saturday, there was a 10-year anniversary of the symbolic beginning of the global financial crisis. So it’s a great opportunity to discuss lessons from the Lehman’s collapse and the post-crisis legacy for the gold market.

Too Little Capital

10 years ago, Lehman Brothers collapsed, which is commonly considered as a symbolic beginning of the Great Recession. We analyze thoroughly lessons from the Lehman’s bankruptcy for the gold market in the upcoming October edition of the Market Overview. But it is such a vast and important topic that we decided to write about it today as well. In contrast, we will focus on what we have not learned from Lehman Brothers’ collapse.

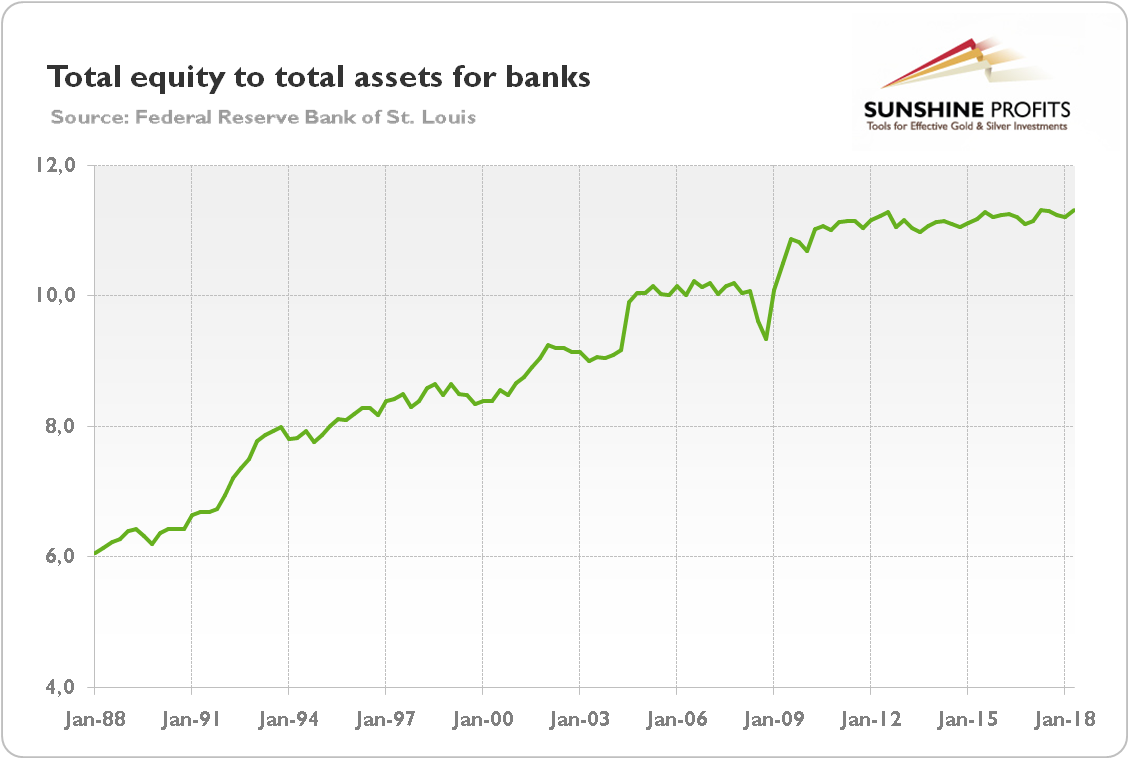

In short: the global financial crisis was caused by excessive indebtedness. Banks had too much debt and too little equity, so they couldn’t bear the losses they faced. But little has changed. Sure, the commercial banks were recapitalized, but the financial system remains generally fragile like back in 2007-2008. As the chart below shows, the total equity to total assets is 11.3 percent. It is more than one percentage point higher than banks had had on the eve of the crisis in 2008, but it is not enough, by any reasonable measure (especially that the weighted average tangible common equity ratio at the six largest U.S. banks is even lower). The implication for gold is clear: when another crash comes, it may quickly transform into a banking crisis, if banks do not have adequate capital. Gold will shine then.

Chart 1: Total equity to total assets for US banks from Q1 1988 to Q2 2018.

Too Much Debt

The pre-crisis boom was fueled by easy money and low interest rates. Even people with no income, no assets and no job were given loans. As a result, the global debt surged from $84 trillion at the turn of the century to $173 trillion at the time of the 2008 financial crisis. The problem is that 10 years after the collapse of Lehman Brothers, due to the ZIRP, the global debt ballooned to $250 trillion. We may call it the post-Lehman legacy.

Leave A Comment