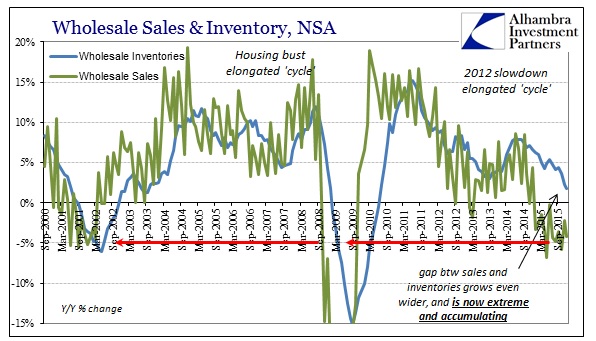

The wholesale level of the supply chain continued its divergence, though it seems increasingly likely that inventories have at least rolled over even if they are still building. Sales fell by 4.2% unadjusted year-over-year while inventories were up only 1.8%. That was the slowest inventory growth since the summer of 2010, but it still leaves the inventory gap as unbelievably wide.

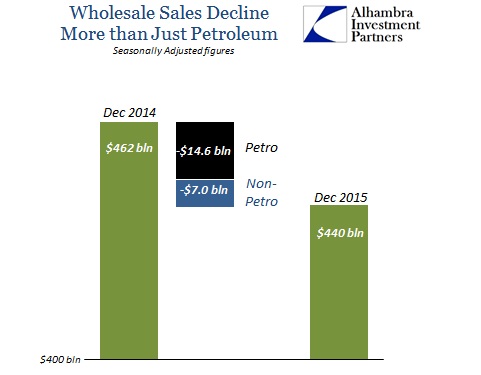

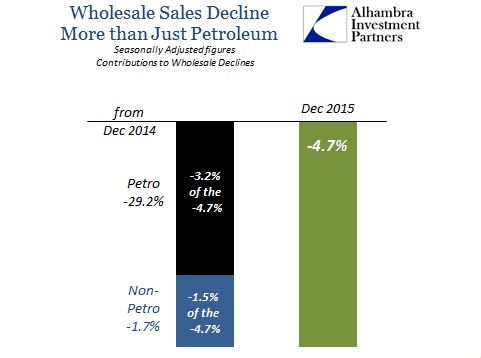

Petroleum is still blamed as the extent of the growing discrepancy, but the wholesale level is broadly shrinking even outside of oil prices. Total wholesale sales were $461.7 billion (seasonally adjusted) in December 2014 but only $440.0 billion in December 2015. Of that $21.6 billion decline, wholesale sales of petroleum accounted for $14.6 billion, meaning that non-petroleum sales declined by just less than $7 billion. A healthy economy produces +5% to +10% in wholesale growth with or without oil, so sales growth overall ex petroleum less than that is concerning; -1.7% is downright recessionary.

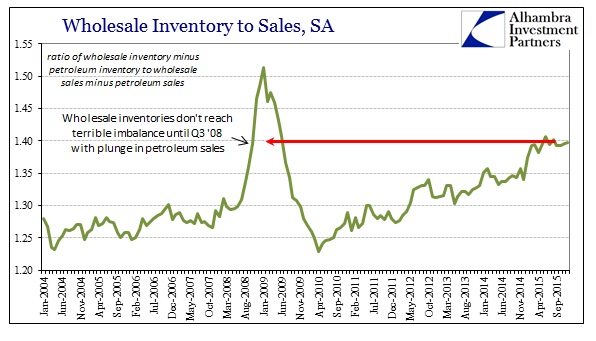

Wholesale sales ex petroleum had been flat since late 2014 (concerning), but have in the past few months started to decline precipitously (recessionary). That would suggest that inventory levels non-petroleum are starting to feed into the overall decline as the inventory-to-sale ratio remains significantly elevated but hasn’t grown appreciably worse. In other words, the economy may be working out of that pre-recessionary adjustment phase into more traditional recession footing. Given the extreme in inventory, that is not a particularly welcome transition except as it may represent the inevitable.

The problem, again, is the scale of the inventory imbalance; we have never seen anything like this before. The oil sector and petroleum is clearly contributing to the divergence, but the length and breadth of the inventory departure is far more than that and far more than historical precedence. In the past, wholesale sales and inventory enjoyed a close relationship which only makes sense. Recessions were any sustained divergence between them, as sales declining would produce a lagged effect on inventory (down and up). Historically, that lag has been rather short, at least in comparison to now, as recession typically took the “V-shape.” Businesses tend to liquidate once the overall impression and environment turns.

Leave A Comment