Before I get into a discussion of the latest market action, I will make a clarification of an aspect which I wasn’t aware of. As I have mentioned a few times in the past few weeks, the NY Fed’s Nowcast Q1 GDP growth estimate and the Atlanta Fed’s Q1 GDP Now growth estimate are far apart. Currently the NY Fed model is forecasting 2.8% growth in Q1 and the Atlanta Fed model is projecting a meager 0.6% growth rate. I stated I didn’t have the data on past instances when they diverged to determine which model is likely to be more accurate. The historical data wouldn’t matter as each quarter is different. The better way to determine which model is going to be more accurate is to look at why they are differing.

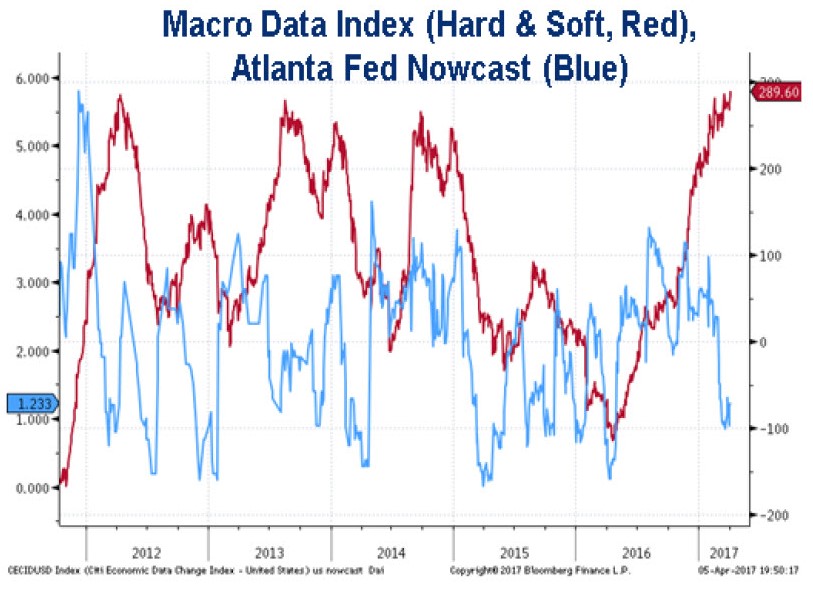

The reason they are differing is because the NY Fed tries to link econometrically soft survey data like consumer confidence, ISM, and the Philly Fed, to a GDP estimate. The NY Fed model includes a much larger percentage of linked estimates from soft data than the Atlanta Fed’s model does. The chart below shows the recent large gap between the soft data and the Atlanta Fed’s forecast. We are once again back to battle between soft and hard data. There is no way to prove whether the soft or hard data will be correct in predicting medium term growth, but for this quarter, the Atlanta Fed will be more accurate since sentiment has no weighting in the GDP report. The one thing sentiment effects is how the market responds to the GDP report. The next report will be weak, so it will be one of the toughest challenges the bull market will face since the start of the year.

Moving into the market’s action on Tuesday, the ten-year bond yield fell sharply to 2.299%. The yield is now down 6.64% year to date. The increase in the yield from the all-time low of 1.3180% may have been a head fake. The reflation trade isn’t working as long-bond bears who were betting on the improving sentiment indicators are paying dearly for their miscalculation. Tying in with the earlier point, the rally in the ten-year bond is consistent with the Atlanta Fed’s forecast for low growth in Q1. The chart below shows the bullish case for equities as the bulls are expecting investors to rotate money from bonds into stocks. That certainly hasn’t happened lately. The increase in both since 2009 gives you a taste for how much liquidity is sloshing around. If there is a rotation into stocks, record PE multiples may result.

Leave A Comment