What to do? This is not as an innocuous question as one might think. For most American families, who have to balance their living standards to their income, they face this conundrum each and every month. Today, more than ever, the walk to the end of the driveway has become a dreaded thing as bills loom large in the dark crevices of the mailbox.

In a continuation of last week’s discussion on consumer debt, the conundrum exists because there is not enough money to cover the costs of the current living standard.

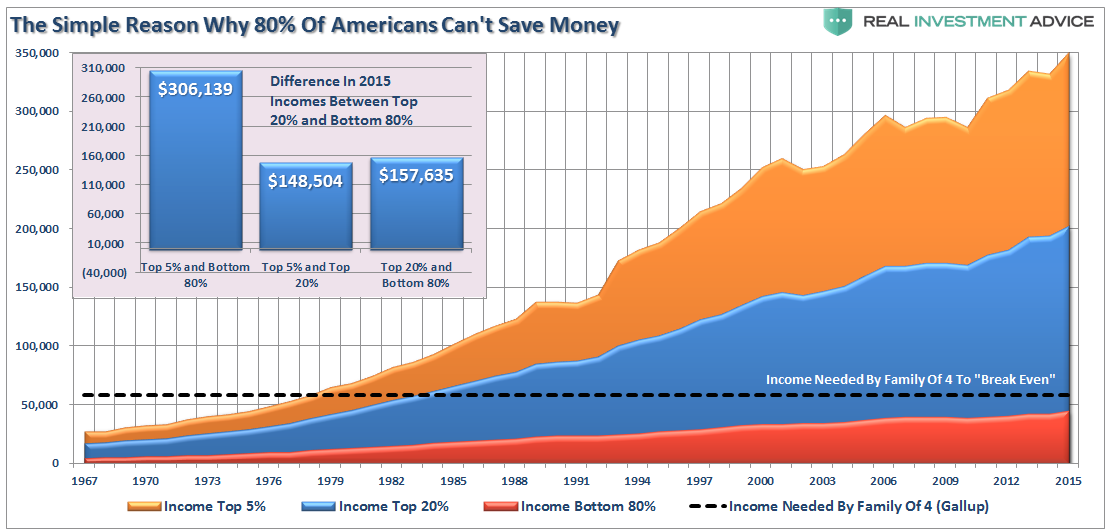

“The average family of four have few choices available to them as discretionary spending becomes problematic for the bottom 80% of the population whose wage growth hasn’t kept up with the standard of living.”

The burden of debt that was accumulated during the credit boom can’t simply be disposed of. Many can’t sell their house because they can’t qualify to buy a new one and the cost to rent are now higher than current mortgage payments in many places. There is no ability to substantially increase disposable incomes because of deflationary wage pressures, and despite the mainstream spin on recent statistical economic improvements, the burdens on the average American family are increasing.

Nothing brought this to light more than the recent release of the Fed’s Report on “The Economic Well-Being Of U.S. Households.” The overarching problem can be summed up in one chart:

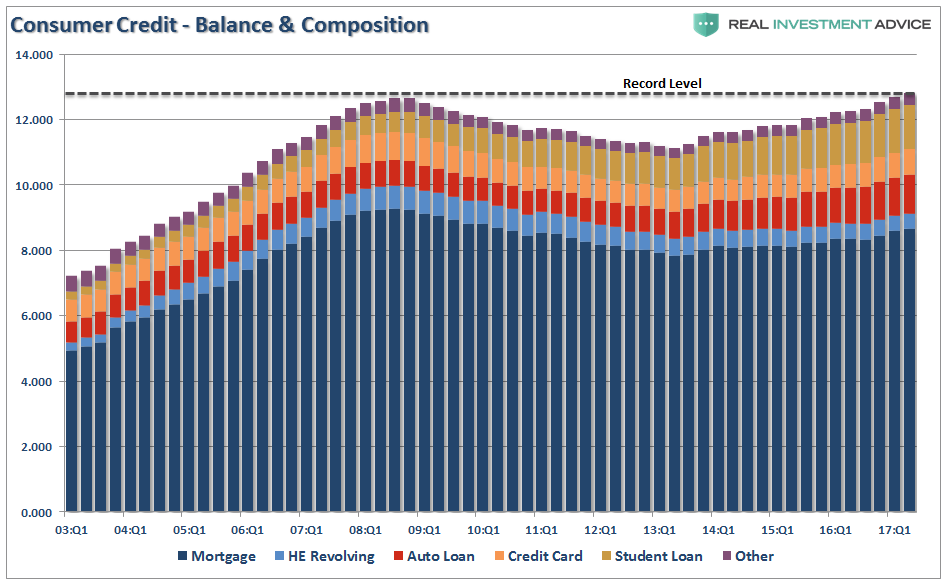

Of course, the recent rise in consumer credit to all-time highs supports that analysis.

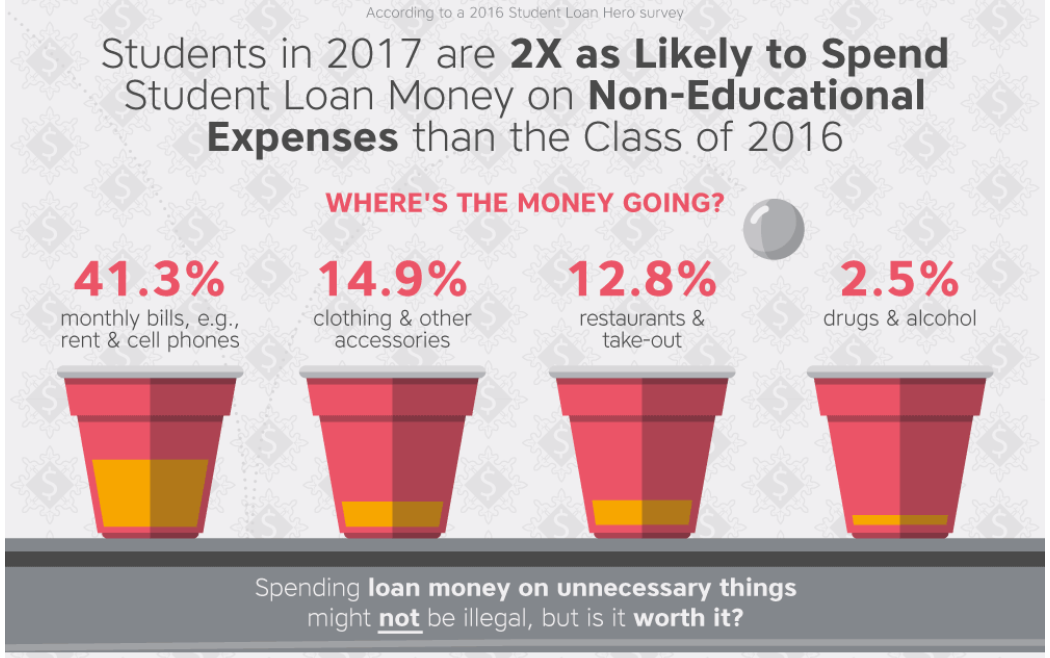

Don’t be fooled by the rise in “student loan” debt either. That is NOT representative of a mass hoard of individuals all clamoring into classrooms across the country to garner the benefits of higher education. According to a 2016 Student Loan Hero survey, individuals have other plans for student loan funds which are easy to acquire.

Or as Bloomberg noted in their survey, 1-in-5 American students will use their student loans to pay for expenses such as vacations, dining out and entertainment. To wit:

Leave A Comment