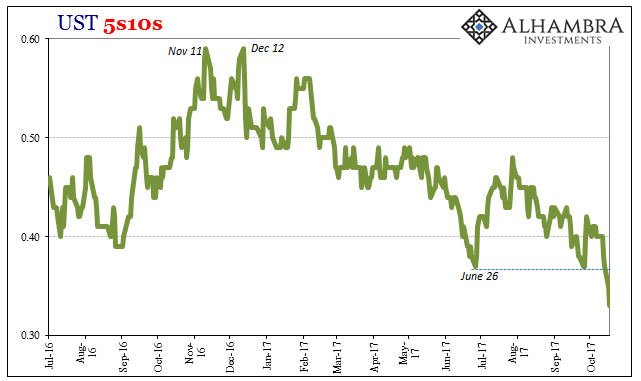

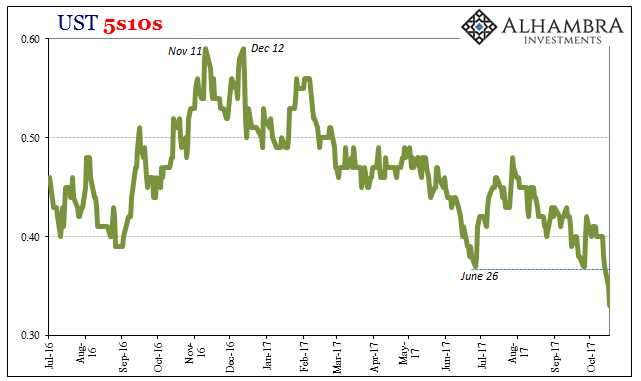

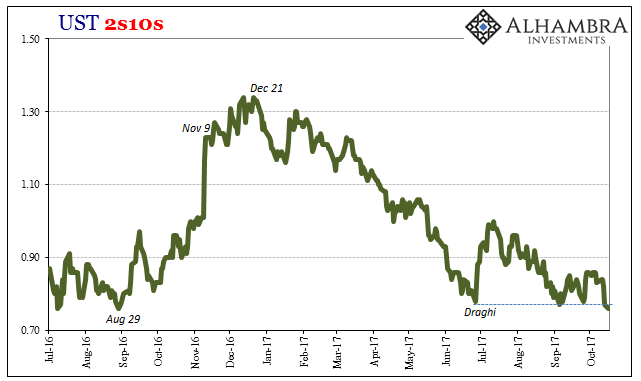

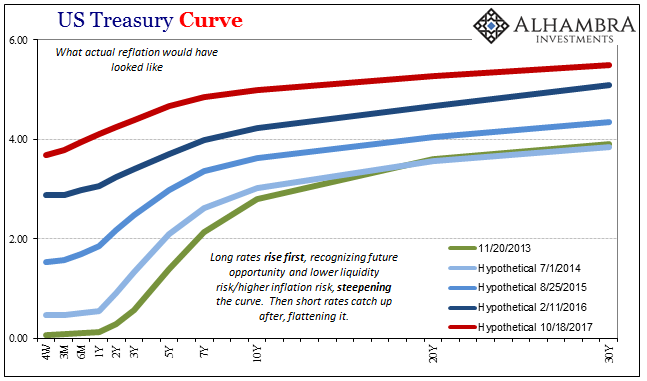

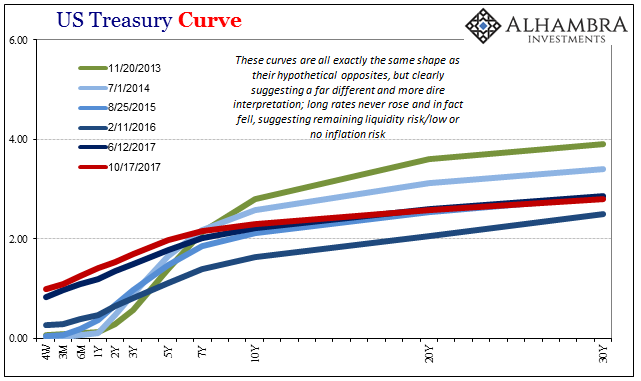

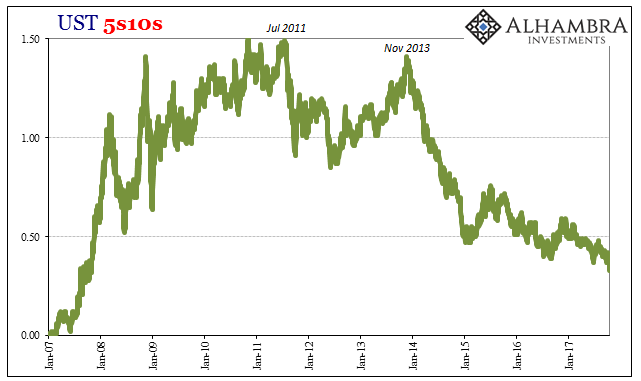

At this point in the longer term process of unwinding the Fed’s prior emergency activities, the yield curve was supposed to flatten. That was the plan all along. If monetary policy was successful, or had even run into just dumb luck somewhere in the last ten years, here where policymakers declare the economy to be short rates would be moving faster than those at the long end.

The flattening is taking place, to be sure, and more so over recent weeks. But it isn’t the same process as would have defined success and recovery; it is instead the opposite indication.

Actual recovery would have been predicted by long rates. Sensing a real reduction in liquidity risk in combination with higher inflation risk (both of which equal out to higher economic opportunity), long rates would have risen faster first, well ahead of short rates stuck at or near zero. The resulting steepening would have been a very positive sign; as it was taken to be in Reflation #1 and Reflation #2 (Reflation #3 was appreciably less so).

But those prior “reflations” were incomplete, or at the very least interrupted. They never got nearly far enough, as the market recognized instead that the basis for them was really lacking (and to some degree more emotion than rational analysis; this last one was surely almost all the former, which is why it remained so small and therefore rational by comparison). As a result, the yield curve twice re-compressed (flattened) prematurely (from the policy perspective) as long rates came back down.

In this third “reflation”, long rates have been more steady while short rates are now moving (in historical comparison still very slowly). The result is the same for the curve, and it’s the opposite of what recovery would look like. The treasury curve is compressing again and to new low levels because it is telling the world that nothing has changed other than the Fed’s attempt to redraw the short-term frame of reference.

Leave A Comment