There are a handful of movies that suck me in whenever they come around. Goodfellas. The Godfather. The Shawshank Redemption.

Still, there’s only one production where I can never get enough of the main character’s outlandishness. Melvin Udall in As Good As It Gets. He hoards bars of soap as part of an obsessive-compulsive disorder. He sneeringly berates a woman for admiring his work as an author. He even shoves the neighbor’s dog down a laundry chute.

I watched the Jack Nicholson portrayal for the “umpteenth” time this past weekend. Shortly thereafter, I found myself thinking about one of the character’s signature lines: “What if this is as good as it gets?” Melvin Udall was talking about life itself. Me? I wondered whether or not we’re near the top of the bull market’s eight-year ride.

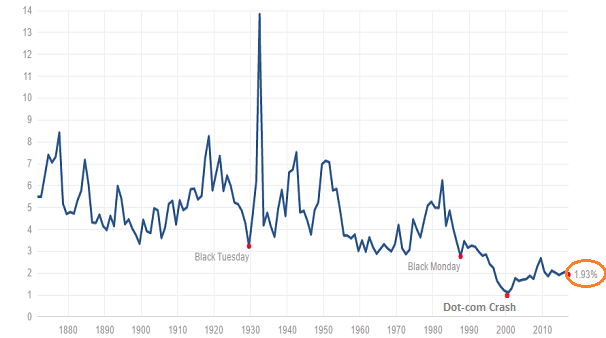

The S&P 500’s dividend yield as well as it’s earnings yield (E/P) are near historic lows. That may not have meant as much in 2016 when the risk-free 10-year Treasury notes yielded between 1.50% and 1.75%. At the moment, though, the 10-year Treasury is offering 2.56%.

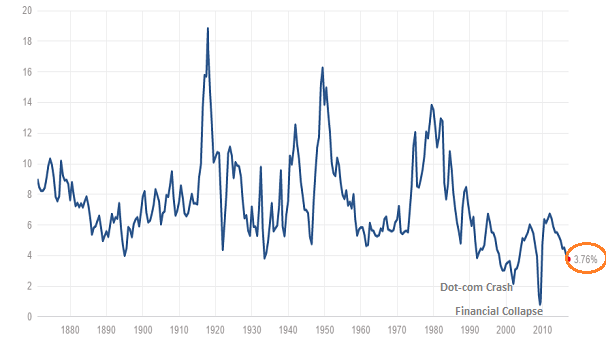

The equity risk premium (ERP) – the excess return for investing in stocks rather than comparable government obligations – is a piddling 1.20% (3.76%-2.56%=1.20%). That is precious little reward for a whole lot of potential risk of financial loss. Worse yet, in nearly 150 years of data, the earnings yield (E/P) was only lower during the tech wreck (2000-2002) and the financial crisis (2008-2009).

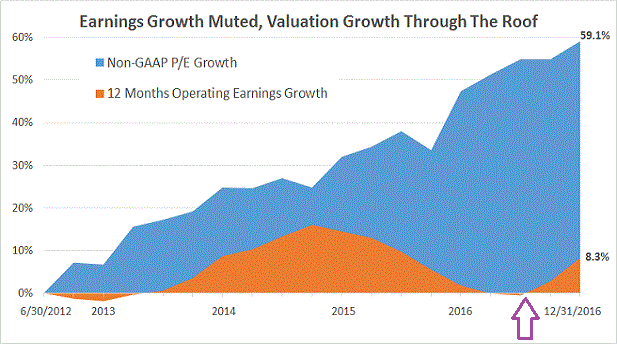

In addition to exceptionally meager dividends, S&P 500 corporations have barely grown bottom line profits since mid-2012. Nearly all of the stock price appreciation over the last four-and-a-half years came with total operating earnings growth of just 8.3%.

The good news? Earnings growth may be back in style. According to FactSet estimates, we should expect corporations to celebrate double-digit earnings growth (10%-plus) in calendar year 2017.

Leave A Comment