Written by Ambrose Evans-Pritchard, The Telegraph

The US credit markets are flashing a rare warning of economic trouble ahead, signalling that the Federal Reserve risks blundering into another recession without a deft change of course.

A blizzard of surprisingly poor data across the world suggests that the Fed’s liquidity squeeze is taking a greater toll than widely assumed, and that the institution’s staff model has so far failed to pick up the danger signs.

US jobs growth fizzled to stall-speed levels of 103,000 in March. The worldwide PMI gauge of manufacturing and services has dropped to a 14-month low. The average “Nowcast” tracker of global growth has slid suddenly to a quarterly rate of 3.2pc from 4.1pc as recently as early February.

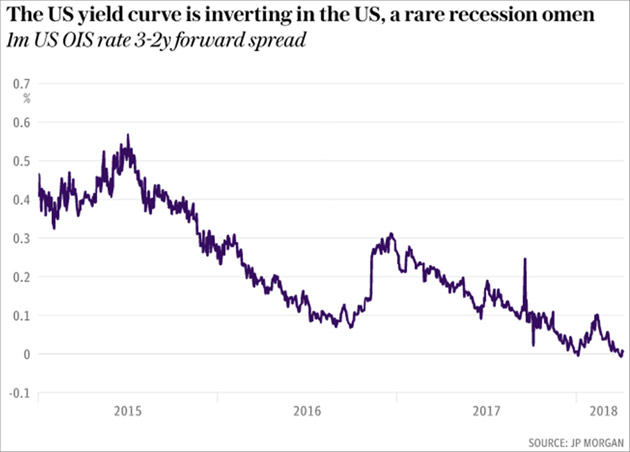

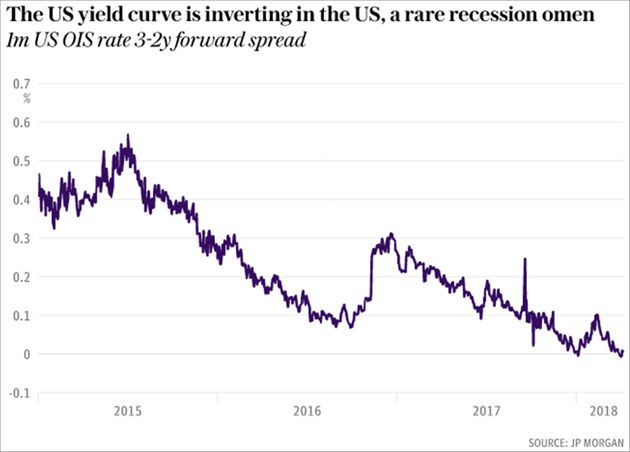

Analysts at JP Morgan say the forward curve for the one-month Overnight Index Swap rate (OIS) – a market proxy for the Fed policy rate – has flattened and “inverted” two years ahead. This is a collective bet by big institutional investors and fund managers that interest rates may be falling by then.

It is a market verdict that Fed officials have lost touch with reality in thinking that they can safely raise rates another seven times to 3.5pc by late 2019, as implied by the “dot plot” forecast. It is tantamount to a recession warning.

“An inversion at the front end of the US curve is a significant market development, not least because it occurs rather rarely. It is generally perceived as a bad omen for risky markets,” said Nikolaos Panigirtzoglou, JP Morgan’s market strategist.

“Markets have started pricing in a Fed policy mistake or have started pricing in end-of-cycle dynamics,” he said. Both possibilities are disturbing.

The OIS yield curve has inverted three times over the last two decades. In 1998 it proved to be a false alarm because the Greenspan Fed did a pirouette and flooded the system with liquidity. In 2000 it was a clear precursor of recession. In 2005 it signaled that the US housing boom was already starting to deflate.

Leave A Comment