Have you been eager to see how Wells Fargo & Company (WFC – Free Report) performed in Q3 in comparison with the market expectations? Let’s quickly scan through the key facts from this San Francisco-based money center bank’s earnings release this morning:

In line Earnings

Wells Fargo came out with adjusted earnings per share of $1.04, in line with the Zacks Consensus Estimate. Results excluded mortgage-related litigation accrual.

Lower revenues and higher expenses were recorded.

How Was the Estimate Revision Trend?

You should note that the earnings estimate for Wells Fargo depicted optimism prior to the earnings release. The Zacks Consensus Estimate has increased around 1% over the last seven days.

Also, Wells Fargo has an impressive earnings surprise history. Before posting in-line earnings in Q3, the company delivered positive surprises in all the prior four quarters. Overall, the company surpassed the Zacks Consensus Estimate by an average of 2.99% in the trailing four quarters.

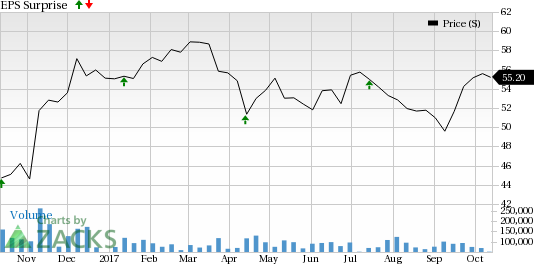

Wells Fargo & Company Price and EPS Surprise

Revenue Came In Lower Than Expected

Wells Fargo posted revenues of $21.9 billion, lagging both the Zacks Consensus Estimate of $22.3 billion as well as the year-ago number.

Key Stats to Note:

What Zacks Rank Says

The estimate revisions that we discussed earlier have driven a Zacks Rank #3 (Hold) for Wells Fargo. However, since the latest earnings performance is yet to be reflected in the estimate revisions, the rank is subject to change. It all depends on what sense the just-released report makes to the analysts.

Leave A Comment