For whatever reasons — capital outflows, PBoC non-intervention — the yuan has depreciated substantially since the Trump administration has announced Section 301 actions against China. This has implications not just for the CNY/USD exchange rate, but also other East Asian currencies.

It’s interesting to note how the overall US trade-weighted dollar against a broad basket of currencies comoves with the CNY/USD exchange rate.

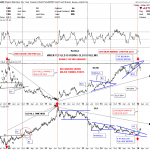

Figure 1: Nominal trade weighted US dollar (blue, left log scale), up is dollar appreciation; and CNY/USD exchange rate (red, right log scale), up is dollar appreciation against CNY. Source: FRED.

Over the sample period, the correlation between the two series is positive and statistically significant. Each one percentage point depreciation of the yuan against the dollar was associated with a 0.88 percentage point appreciation of the broad trade weighted dollar. The adjusted R2 is 0.36.

This association — representing a clearly non-structural parameter — is suggestive, but does not answer the question of what happens to other currencies when the CNY depreciates. In Chinn (2014), I found that post-2005, increasing evidence of a regional RMB zone, which made sense given the development of global supply chains involving China. However, by now those results are very out of date. A more recent assessment is by McCauley and Shu (2018) (presented earlier at this conference):

The key message of our analysis is that it is premature to declare a stable renminbi zone, defined as a set of jurisdictions with currencies that share more than half of the renminbi’s movements against the dollar (ie for which ?1 exceeds 0.5). Such a zone has the force of trade links, business cycle correlations and possibly increased financial links behind it, but it evidently depends on a multilateral and predictable management of the renminbi’s exchange rate. In the period since May 2017, our estimates of ?1 suggest a strictly northeast Asian renminbi zone.

Leave A Comment