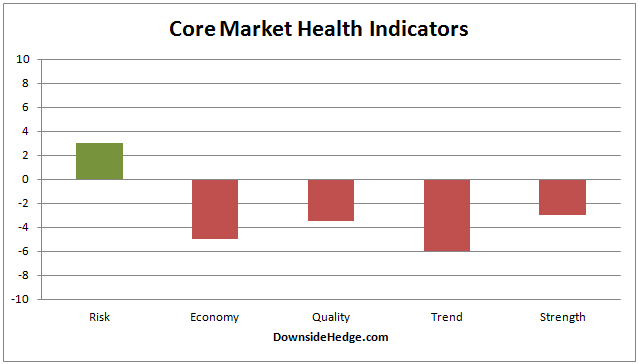

Over the past week most of my core measures of market health improved. Most notably is that my measures of risk went positive.

This changes the portfolio allocations as follows:

Long / Cash portfolio: 20% long and 80% cash

Long / Short Hedged portfolio: 60% long high beta stocks and 40% short the S&P 500 Index (or the ETF SH)

Volatility Hedged portfolio: 100% long (from 10/9/15)

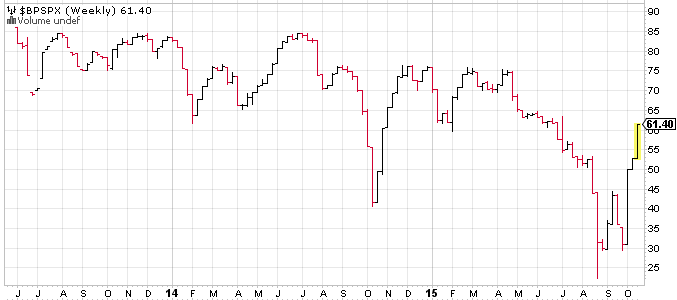

Another thing of note this week is that the Bullish Percent Index (BPSPX) is back above 60%. This reduces the risk of a steep or waterfall type decline. Here’s a post that explains the risk associated with poor breadth in the market.

Related Posts

‘Do not delay’ — ASIC warns Aussies to look for 10 signs of a crypto scam

‘Do not delay’ — ASIC warns Aussies to look for 10 signs of a crypto scam The Media Strikes Back Against Facebook

The Media Strikes Back Against Facebook First Look At January: ADP Says 234K New Nonfarm Private Jobs

First Look At January: ADP Says 234K New Nonfarm Private Jobs WTI Crude Oil And Natural Gas Forecast – Tuesday, September 5

WTI Crude Oil And Natural Gas Forecast – Tuesday, September 5 Weekly Gasoline Price Update: Regular And Premium Down

Weekly Gasoline Price Update: Regular And Premium Down- US Business Cycle Risk Report – 17 March 2016

Leave A Comment