The 10-year Treasury rate has broken out.In less than two months, it has jumped 44 basis points.Equities are selling off.But how sustainable is the rise in these yields, given the leverage in the system?

Chart 1 is causing a lot of stir and anxiety among equity investors.Or, they were simply looking for an excuse to sell off, and found one in the recent surge in rates.

The 10-year yield (3.23 percent) bottomed in July 2016 at 1.34 percent, and has since been making higher lows.In September last year, these notes were yielding 2.03 percent.Most recently, yields were 2.81 percent on August 22, then rising to 3.25 percent by last Friday.That is a jump of 44 basis points in less than two months.

Wednesday last week, the 10-year rate broke past the mid-May high of 3.12 percent.This resistance goes back to at least June 2003.The last time the 10-year unsuccessfully tried to take out three-plus percent was five years ago.Then in April this year, it again went after that ceiling, which finally gave way six sessions ago.

Arguably, this now opens up room for yields to head much higher.At least this sentiment is driving action in stocks, which are getting pummeled.

Fundamentally, there is a lot to argue for higher rates.

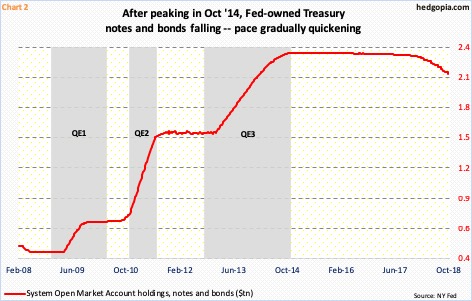

The Fed, for one, is cutting back on its Treasury holdings.Post-financial crisis, it began purchasing Treasury and mortgage-backed securities.During three iterations of quantitative easing, holdings of notes and bonds went from just north of $400 million in November 2008 to $2.35 trillion in October 2014.As of last week, this was down to $2.14 trillion (Chart 2).Beginning this month, reduction of these notes and bonds can be as high as $50 billion/month.This can begin to matter.

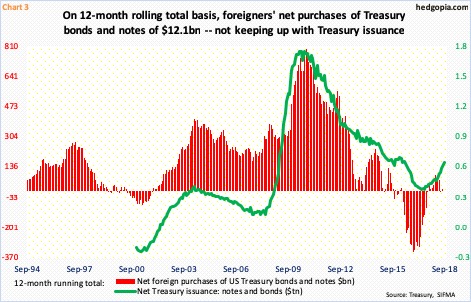

Foreigners of late have turned lukewarm toward US sovereign bonds.On a 12-month rolling total basis, they purchased $12.1 billion worth of Treasury bonds and notes in July.This dropped from purchases of $92.2 billion as recently as February.

Historically, foreigners’ purchases tend to follow issuance of Treasury securities (Chart 2).This time around, there has been a slight divergence.

Leave A Comment