Back in the 1990s, processor speeds doubled nearly every year. As we hit the most recent decade, the increases in processor performance slowed the rate of real development to a crawl. What’s most interesting during this time period is the rise and fall of companies in the technology sector. Intel, being the behemoth that it is, weathered the storm fairly well, with some struggles until the last few years. NVIDIA was nearly left for dead until machine learning gave the graphics card maker a new life. Yet, still in the back sits Advanced Micro Devices.

Despite a general pickup in the overall technology sector, AMD has lagged its competitors substantially over the years. While revenues picked up nicely from 2015 through recent, the EPS failed to break into positive territory until 2017. True, the company has improved its net margins. However, it lags woefully behind its competitors and has only recently turned cash flow from operations positive in the last couple years. The company sits in a growing market but has a long way to go before they can justify their current or higher share prices.

Margin Mayhem

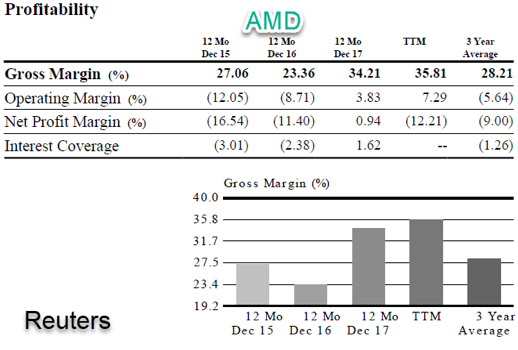

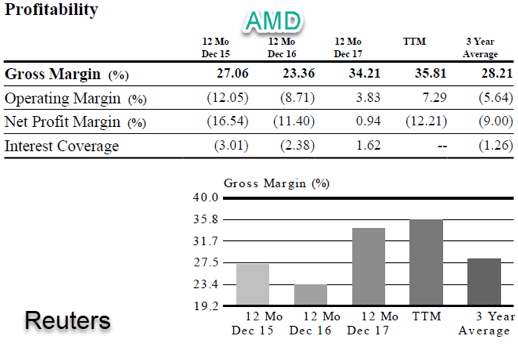

Bulls who cover AMD point to the sizable growth in the gross margin, which is nothing to sneeze at. From 2015 to present the gross margin has jumped a sizable 7%+. The Operating Margin and Net Margin ratios have all turned around as well. Yet, compare that to Intel & NVIDIA. Relatively speaking, they aren’t even close. NVIDIA boasts a Net margin of that’s grown from just under 16% to 33%, while Intel has increased from just over 15% last year to a TTM of nearly 28%. The operating margins of both are nearly double that of AMD.

All that being said, the earnings still show a significant disparity. Intel sits at a P/E of 12.2, which is pretty solid for a company that’s been growing both it’s revenues and margins and a sizable clip while plowing a lot of money back into the business for research. NVIDIA is priced a bit higher with a P/E of 44.61. If we took the most recent quarter earnings for AMD and did a run rate, the P/E would still be over 40. However, the caveat remains: If the company manages itself into the same fundamentals as Intel and NVIDIA, while capturing market share, then their current share price becomes more fairly valued.

Leave A Comment