Upon the precipice of the Great “Recession”, US workers were cushioned to some extent by what economists call sticky wages. Before the Great Depression, as well as during it, companies would attempt to deal with looming economic contraction by cutting pay rates before workers. Nowadays, the intent is reversed; businesses will try to keep core workers by keeping pay rates as steady as possible while instead shedding extraneous employees at potentially a furious pace (see: 2008-09).

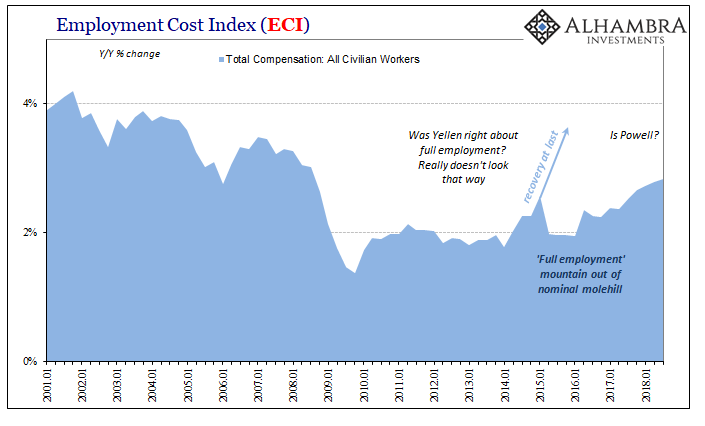

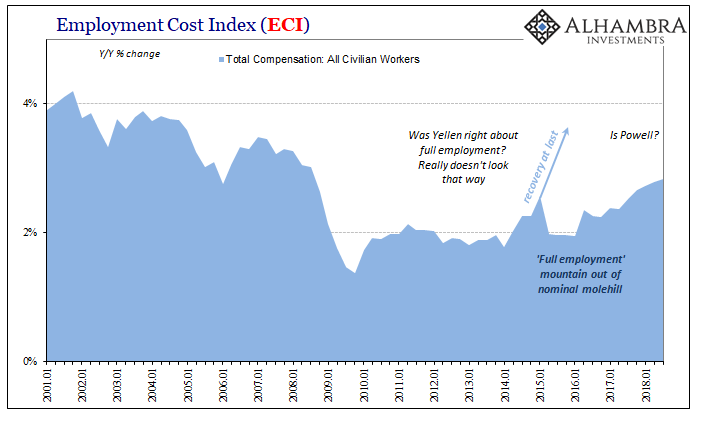

The Bureau of Labor Statistics’ (BLS) Employment Cost Index (ECI) captures sticky wages pretty well. In the fourth quarter of 2007, just as the contraction was beginning, that measure of labor costs rose 3.3% year-over-year. That was down only a bit on average, where costs were growing at about 3.6% since the dot-com recession had ended.

Even as the contraction gained momentum, the ECI kept growing at least 3% until the worst of it. Even though the unemployment rate had jumped from 4.7% to 6.1% by the time of the panic, employment cost growth remained pretty stable. It wasn’t until the monetary deluge in Q4 2008 that wage rates finally stalled. They never really contracted, at the lowest it was still +1.4% by the end of 2009 toward the end of the mass layoff period.

Sticky wages work in the other direction, too. Salary increase rates will stay low until business factors shift substantially. These tend to be cyclical and macro. This is the fuss about the unemployment rate. A tight labor market can shift employment costs; an extraordinarily tight labor market should shift employment costs.

According to the latest figures from the BLS, the ECI increased 2.83% year-over-year in the third quarter of 2018. This was the largest gain in aggregate employment costs since Lehman Brothers and AIG. And that’s what has been broadcast over and over today; the highest in ten years!

But 2.83% is still tepid, that’s the reality. If the ECI increased 3.02% during the very same quarter as Lehman and AIG, nine months into a pretty substantial contraction to that point, what is 2.83%? It sure doesn’t indicate a tight labor market, it’s not even that good.

Leave A Comment