Historically, dividend growth investing has been one of the best ways for regular people to compound their wealth and income over time.

Of course, the trick is to be able to carefully select the best quality companies, those with high-quality management teams, strong balance sheets, predictable businesses, and dividend-friendly corporate cultures.

That’s why dividend aristocrats have become a favorite among income investors, because with their long-term (25+ years) streaks of annual dividend growth, aristocrats can be a great starting place to look for the kind of steady blue chips that have done so well in the past.

Investors can learn more about all of the dividend aristocrats here.

Let’s take a look at Archer Daniels Midland (ADM), one of the oldest and most time-tested members of this group (with 41 straight years of payout growth to its name), to see if this boring agricultural giant might be appropriate for a diversified dividend growth portfolio. Especially with shares offering a dividend yield that is near its highest level in 20 years.

Business Overview

Founded in 1898 in Chicago, Illinois, Archer Daniels Midland is one of the world’s largest food procurers, transporters, storage, processors, and sellers of agricultural commodities and products through its global network of processing plants, storage facilities, and transportation vehicles.

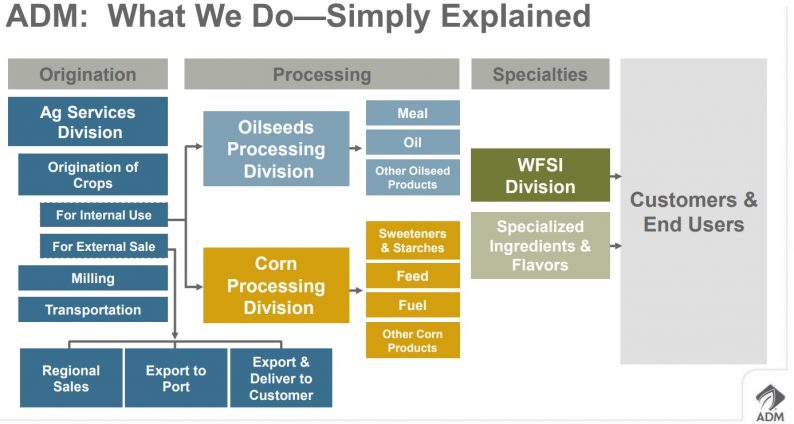

Or more simply put, ADM helps to feed the world, thanks to its immense business and geographic diversification. Some of the company’s end products include vegetable oil, protein meal, flour, corn sweeteners, starch, ethanol, and other food and feed ingredients.

Source: Archer Daniels Midland Investor Presentation

The company has four main business segments:

Business Analysis

Archer Daniels Midland has been in business for more than 100 years and isn’t going away anytime soon thanks to several competitive advantages.

Most notably, Archer Daniels Midland’s core operations – procuring, storing, processing, and selling various agricultural commodities – are extremely capital intensive. The company has the largest grain terminal and shipping network in the country and maintains hundreds of processing plants and storage facilities around the world, for example.

These capabilities allow Archer Daniels Midland to be the lowest cost and fastest provider of its commodities and processed products to many customers’ facilities, where it delivers directly.

Replicating the company’s physical footprint; fleet of trucks, trailers, tank cars, river barges, towboats, and vessels used to transport its products; and its logistical expertise would be nearly impossible. With razor-thin operating margins in this commodity industry, there is no room for inefficiencies.

At the end of the day, the basic investment thesis for food companies such as Archer Daniels Midland is simple: everyone has to eat. That’s especially true with a growing global population and with faster-growing emerging markets (such as China) whose middle classes are increasingly consuming more western style diets.

Leave A Comment